Summary

- US Treasury (UST) yields fluctuated in October, with the 10-year yield reaching a 16-year high of 5.02% at one point as data pointed to continued resiliency in the US economy. At the end of October, the benchmark 2-year and 10-year yields settled at 5.09% and 4.93%, respectively, 4.4 basis points (bps) and 36 bps higher compared to end-September. Central banks in Asia took divergent monetary paths, while headline inflation prints registered mixed in September.

- Amid the current rise in oil prices, global central banks have become more vigilant against inflation, becoming increasingly wary of risks occasioned by a potentially premature end to their rate hiking cycles. We therefore deem it prudent to retain a neutral view on duration for most countries in the region. As for currencies, we have a favourable view of the Chinese renminbi and Philippine peso, while we are cautious on the South Korean won and Thai baht.

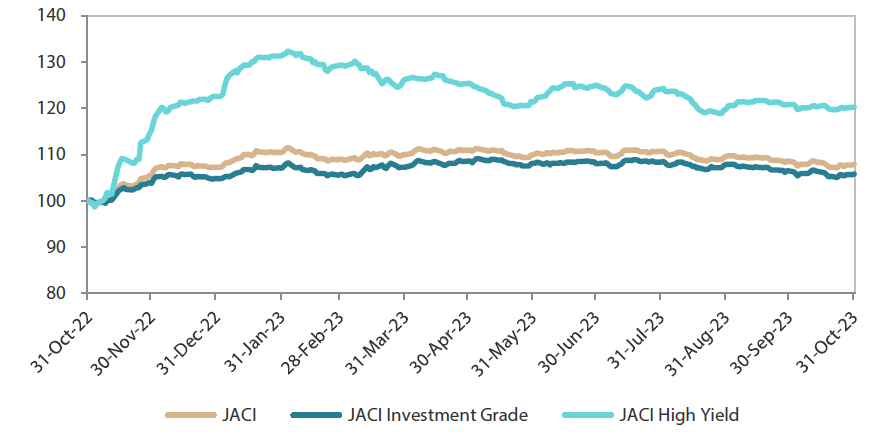

- Asian credits retreated 0.65% in October, despite credit spreads tightening by about 20 bps as UST yields rose. Asian high-grade (HG) credit lost 0.67%, while Asian high-yield (HY) credit retreated 0.51%.

- We expect macro and corporate credit fundamentals across Asia ex-China to stay resilient with fiscal buffers, although slower economic growth appears to loom over the horizon. Asian banking systems remain strong, with their stable deposit base, robust capitalisation and strong pre-provision profitability providing buffers against moderately higher credit costs ahead.

Asian rates and FX

Market review

USTs weaken further in October

UST yields fluctuated in October. A significantly stronger-than-expected US payrolls report at the start of the month bolstered a likelihood of an additional rate hike by the US Federal Reserve (Fed), prompting an initial sell-off in USTs. Investors subsequently sought safe haven assets amid the Israel-Hamas conflict, and yields declined. Dovish Fed speak, with multiple officials pronouncing that the recent spike in long-end yields had done a part of the tightening job, further supported demand for USTs. However, subsequent US data that pointed to continued resiliency in the US economy pushed the 10-year yield to a 16-year high of 5.02%. Over in Europe, the European Central Bank (ECB) kept interest rates on hold, on the assessment that previous rate hikes have increasingly dampened demand and would help soften inflation over time. At the month-end, the Bank of Japan (BOJ) sharply raised its inflation forecasts and further loosened its grip on government bond yields, declaring the 1% ceiling on 10-year yields it had been imposing under its yield curve control scheme as a “reference” point. At end-October, the benchmark 2-year and 10-year UST yields settled at 5.09% and 4.93%, respectively, 4.4 bps and 36 bps higher compared to end-September.

Chart 1: Markit iBoxx Asian Local Bond Index (ALBI)

| For the month ending 31 October 2023 | For the year ending 31 October 2023 | |

|

|

Source: Markit iBoxx Asian Local Currency Bond Indices, Bloomberg, 31 October 2023.

Central banks in the region take divergent monetary paths

Bank Indonesia (BI) and Bangko Sentral ng Pilipinas (BSP) both resumed tightening monetary policy, raising their respective policy rates by 25 bps each, while central banks in South Korea and India stood pat. The Monetary Authority of Singapore (MAS) kept the slope, centre and band width of the Singapore Dollar Nominal Effective Exchange Rate (SGDNEER) unchanged. According to the BSP, the off-cycle move was needed “to prevent supply-side price pressures from inducing additional second-round effects and further dislodging inflation expectations”. It further signalled readiness to deliver “follow-through policy action” if necessary. In Indonesia, BI Governor Perry Warjiyo said the 25-bps hike was a “pre-emptive, forward-looking” step to mitigate the impact of imported inflation risks. At the same time, the bank sees the rate hike supporting the stability of the Indonesia rupiah. Meanwhile, the Reserve Bank of India (RBI) held its policy rate steady, with the policy committee saying it remains focused on the withdrawal of accommodation. The RBI also announced potential open market operations sales to mop up any build-up of excess liquidity, with no details given on the timing or size of these. Elsewhere, the MAS said that prospects for growth are “muted in the near term”, and projects growth to expand “closer to its potential rate” in 2024. It also announced a shift to quarterly monetary policy meetings from 2024, with the next policy statement to be released in late January 2024.

Headline inflation prints mixed in September

Overall inflation prints in South Korea, Singapore and the Philippines rose, while those in India, Malaysia, Thailand and Indonesia moderated. The Philippines’ inflation rate climbed to 6.1% year-on-year (YoY), driven primarily by a sharp rise in prices of food and transport. This was much higher than the 5.3% increase in August. Stripping out volatile components of the consumer price index (CPI), core inflation eased to 5.9% YoY in September from 6.1% in August. In Singapore, overall inflation also edged higher, to 4.1% YoY in September from 4.0% in August, as a pickup in private transport inflation more than offset the decline in core and accommodation inflation. Meanwhile, price pressures in Malaysia eased, with the rise in the headline CPI index moderating to 1.9% YoY from 2.0% in prior month, prompted partly by easing food and transport inflation. Similarly, the rise in Indonesia’s headline inflation number moderated to 2.28% YoY in September from 3.27% in August, prompted mainly by high base effects from fuel price hikes in 2022.

China’s data suggest some economic stabilisation; policymakers step up support for economy

China’s economy slowed less than expected in the third quarter of 2023. The 4.9% YoY GDP increase suggests that the economy is on track to meet the government’s full-year 2023 growth target of “around 5%”. Activity data in September supported the view that the economy may be stabilising. Retail sales grew 5.5% YoY in the month from 4.6% in August and industrial production increased 4.5% YoY, matching August’s pace. Meanwhile, fixed asset investment growth rose 3.1% YoY in the January to September period, weaker than the 3.2% expansion over the first eight months of the year. The property slump remained a drag on the economy, with property investment growth declining 9.1% YoY in the first nine months of the year, outpacing the 8.8% decline in the January to August period. Separately, Chinese banks issued more loans in September, heeding policymakers’ call to boost lending to support a recovery. A marked increase in mortgage loans was the main driver of the rise in new loans, driven by policy easing, but whether it is sustained remains to be seen. Aggregate financing stood at Chinese yuan (CNY) 4.12 trillion in September, on the back of a jump in new government bond financing.

Towards the month-end, the government stepped up support for the economy, announcing that it will issue CNY 1 trillion additional sovereign debt, effectively lifting the 2023 fiscal deficit ratio to “around 3.8% of GDP”, above the 3% set in March. That the funds will be fully transferred to local governments (half in 2023 and half in 2024) shows that the central government is willing to step up support to help resolve the local government debt issue. Separately, People's Bank of China (PBOC) Governor Pan Gongsheng vowed to make policy more targeted and forceful.

Market outlook

Maintaining a neutral duration stance; prefer Indian bonds

UST yields are being lifted by elevated oil prices and increasing expectations that interest rates will remain high for longer than previously anticipated. Amid rising oil prices, global central banks have become more vigilant against inflation, becoming increasingly wary of risks occasioned by a potentially premature end to their rate hiking cycles. Consequently, we deem it prudent to retain our neutral view on duration for most countries in the region.

India government bonds are now officially included in JP Morgan’s Government Bond Index-Emerging Markets (GBI-EM) Index and will be the second biggest emerging market country in the index by April 2025. This may provide solid support for Indian government bonds vis-à-vis regional peers over the short and medium term as foreign interest in the market increases. In contrast, Thai government bonds could succumb to further selling pressure on concerns around the size of the new government’s spending.

Chinese renminbi and Philippine peso preferred

The higher-for-longer US rates narrative has prompted another round of broad-based US dollar strength. Within the region, we prefer the Chinese renminbi and Philippine peso, and we are cautious on the South Korean won and Thai baht. Support from the PBOC should be positive for the renminbi, while demand for the peso in the coming months could be underpinned by a seasonal boost. Meanwhile, we expect higher oil prices to be most negative for the current account balances of South Korea and Thailand, negatively affecting demand for their currencies.

Asian credits

Market review

Asian credits retreat in October

Asian credits retreated 0.65% in October despite credit spreads tightening about 20 bps as UST yields rose. The sell-off in USTs prompted Asian HG credit to underperform its high-yield HY counterpart, returning -0.67% despite spreads narrowing by about 3 bps. Meanwhile, Asian HY credit retreated 0.51%, even after spreads tightened 122 bps.

Asian credit spreads traded within a narrow range for most of October, unperturbed by sharp moves in UST yields and the start of the Israel-Hamas conflict. That said, lingering problems for China property and outflows from regional funds continued to weigh on Asia HY prior to a rally on the last trading day. During the month, data out of China added to signs of a stabilising economy. Although the 4.9% YoY third-quarter GDP growth print was lower than the 6.3% expansion in the second quarter, this surpassed the 4.5% rise markets had expected, suggesting that growth is on track to meet the government’s full-year 2023 growth target of “around 5%”. Meanwhile, Chinese banks issued more loans in September, heeding policymakers’ call to boost lending to support the recovery. Towards month-end, the government’s announcement that it will issue CNY 1 trillion additional sovereign debt—effectively lifting the 2023 fiscal deficit ratio well above the 3% set in March—further helped sentiment towards China ex-property credits. Elsewhere, Malaysia and Singapore saw faster YoY growth in the third quarter of 2023, based on advance estimates. The acceleration in Malaysia was driven partly by the services sector, while construction and service-producing industries contributed positively to Singapore’s growth over the period. Overall, spreads of all major country segments—save for China, Taiwan, Indonesia and Malaysia—widened. Macau credits fared the worst, despite positive news flows for China’s Golden Week, as fund outflows and higher UST yields weighed on demand.

UST yields fluctuated in October. A much stronger-than-expected US payrolls report at the start of the month increased probability of an additional rate hike by the Fed, prompting an initial sell-off in USTs. Investors subsequently sought safe haven assets amid the Israel-Hamas conflict, pushing yields to fall. Dovish Fed speak, with multiple officials pronouncing that the recent spike in long-end yields has done part of the tightening job, further supported demand for USTs. However, subsequent US data that pointed to continued resiliency in the US economy pushed the 10-year UST yield to a 16-year high of 5.02%. The ECB held interest rates at 4%, on the assessment that previous rate hikes have increasingly dampened demand and would help soften inflation over time. At the month-end, the BOJ raised its inflation outlook and further loosened its grip on government bond yields, declaring the 1% ceiling on 10-year yields it had been imposing under its yield curve control scheme as a “reference” point. At end-October, the benchmark 10-year UST yield settled at 4.93%, 36 bps higher compared to end-September.

Primary market subdued in October

The primary market was relatively quiet in October, with USD 5.98 billion being raised in the month. Issuers stayed sidelined amid volatility in the rates markets and ahead of the Fed meeting in early November. The HG space saw just nine new issues amounting to USD 4.8 billion, including the USD 2.2 billion four-tranche issue from Korea Development Bank and USD 1.0 billion two-tranche issue from LG Energy Solution. Meanwhile, the HY space had four new issues amounting to USD 1.18 billion.

Chart 2: JP Morgan Asia Credit Index (JACI)

Index rebased to 100 at 31 October 2022

Note: Returns in USD. Past performance is not necessarily indicative of future performance.

Source: Bloomberg, 31 October 2023.

Market outlook

Favourable Asia macro backdrop, stable credit fundamentals creates historical opportunity to lock in yields

The current macro and market backdrop may see little or minor change, with growth expectations for major economies remaining low and some inflation stickiness resurfacing heading into 2024. The resilience of major economies, particularly the US, is prompting the embracing of the “higher-for-longer” narrative for interest rates. While this is weighing on total returns year-to-date, the sell-off in rates is also increasing the attractiveness for investors to lock in historically high all-in yields with yields at post-global financial crisis highs.

The fundamentals backdrop for Asian credit remains supportive. In China, the recent step-up in fiscal measures suggests that policymakers are aware of the challenging environment. This further supports the expectations of policymakers to deliver additional measures to help broaden out the recovery and the determination to boost economic growth in 2024. Macro and corporate credit fundamentals across Asia ex-China are expected to stay resilient with fiscal buffers despite slower economic growth expectation in the first half of 2024. While non-financial corporates may experience a slight weakening in leverage and interest coverage ratios stemming from lower earnings growth and incrementally higher funding costs, we believe there is adequate ratings buffer for most, especially the HG corporates. Asian banking systems remain robust, with a stable deposit base, robust capitalisation and strong pre-provision profitability providing buffers against moderately higher credit costs ahead.

Technically, Asia credit is expected to remain well-supported with lower net new supply as issuers continue to access cheaper onshore funding. Meanwhile, demand remains strong for high quality bonds driven by strong onshore support and pension funds and life insurance companies looking to lock in attractive yields and immunise against long-dated liabilities. Moreover, the consistent outperformance of Asia investment-grade (IG) on a risk-adjusted basis may boost demand and make Asia credit attractive amid the region’s favourable macro backdrop and sufficient fundamental buffer. Key risks include sticky inflation and continued resilience of the US economy, potentially forcing the Fed to continue its hiking policy path, as well as rising geopolitical risks. On the other hand, a sudden and sharp weakening of the US labour market and economic activity, coupled with rising delinquencies and defaults, may push spreads wider across global credit. This could exert some pressure on the valuation of Asia IG credit, which continues to look slightly stretched versus historical levels.