Summary

- US Treasuries (USTs) rallied in December as various data releases continued to support market expectations of the Federal Reserve (Fed) cutting interest rates in 2024. The Fed held steady on rates for a third consecutive time in December and signalled three rate cuts in 2024. At the end of December, the benchmark 2-year and 10-year UST yields settled at 4.25% and 3.88%, respectively, 43.1 basis points (bps) and 44.7 bps lower compared to end-November.

- 2024 looks to be a year of higher returns and lower volatility for Asian local government bonds with UST yields expected to stabilise and start easing. We expect sentiment toward Asia’s bond markets to turn increasingly positive, attracting capital inflows and providing technical support that was largely lacking in 2023. Meanwhile, we believe that the broad theme of stronger Asian currencies against the dollar will dominate in 2024, as we see waning demand for the greenback as the Fed’s rate-hiking cycle comes to an end.

- Asian credits registered strong gains in December as credit spreads tightened about 9 bps and UST yields moved sharply lower. Asian investment-grade (IG) credit returned 2.69% with spreads narrowing about 7 bps, while Asian high-yield (HY) credit gained 2.01%, with spreads tightening about 13 bps.

- We expect macro and corporate credit fundamentals across Asia ex-China to stay resilient due to fiscal buffers although slower economic growth seems to loom over the horizon. Asian banking systems remain strong, with their stable deposit base, robust capitalisation and strong pre-provision profitability providing buffers against moderately higher credit costs ahead. Technically, Asia credit is expected to remain well supported with lower net new supply as issuers continue to access cheaper onshore funding.

Asian rates and FX

Market review

USTs continue to rally in December

USTs extended November’s surge and rallied in December as the Fed moderated its hawkish tone. During the December Federal Open Market Committee (FOMC) meeting, the Fed held steady on rates for the third time in a row, keeping the Fed Funds rate target in a 5.25%–5.50% range. The Fed acknowledged slowing growth and easing inflation in its policy statement; it subtly tweaked its forward guidance, suggesting that the policy rate is at, or close to, peak levels. The latest Fed dot plot now projects the policy rate being reduced by 75 bps over 2024, more than the 50 bps of cuts the previous guidance implied. The latest dot plot also projects the policy rate being cut by 100 bps over 2025 and by 75 bps over 2026. US nonfarm payrolls increased by 199,000 in November, above the estimated 185,000 and marking an uptick from the 150,000 gain in October. The November unemployment rate unexpectedly fell to 3.7% from 3.9% in October. November US consumer prices were largely in line with expectations, with headline inflation coming in at 3.1% year-on-year (YoY) while core inflation was at 4% YoY. At end-December, the benchmark 2-year and 10-year UST yields settled at 4.25% and 3.88%, respectively, 43.1 bps and 44.7 bps lower compared to end-November.

Chart 1: Markit iBoxx Asian Local Bond Index (ALBI)

| For the month ending 31 December 2023 | For the year ending 31 December 2023 | |

|

|

Source: Markit iBoxx Asian Local Currency Bond Indices, Bloomberg, 31 December 2023.

Central banks in India, Indonesia and the Philippines leave policy rates unchanged

Central banks in India, Indonesia and the Philippines kept monetary policy unchanged in December. The Reserve Bank of India (RBI) retained its policy rate at 6.5% for the fifth time in a row. The RBI also maintained its inflation estimate while upgrading its growth forecast—the headline inflation estimate for FY24 was kept at 5.4%, while GDP forecast for FY24 was revised upward from 6.5% to 7%. As expected, Bank Indonesia (BI) kept its policy rate unchanged at 6% for the second straight month. While the policy statement noted the stabilisation of the rupiah and the improving backdrop for capital inflows, BI also emphasised that it would be cautious of "risks that could emerge" and ensure the stability of the rupiah. While BI thinks that the Fed is unlikely to hike further and will cut rates by 50 bps in the second half of 2024, Governor Perry Warjiyo stressed during the post-policy meeting press conference that the central bank will still be "cautious" in its monetary policy stance. Elsewhere, the Bangko Sentral ng Pilipinas (BSP) held the benchmark interest rate steady at 6.50%. According to the central bank, the decision was largely based on the deceleration in inflation over the previous two months. The BSP lowered its inflation forecast for 2024 to 4.2% from 4.4% but left the forecast for 2025 unchanged at 3.4%. Nonetheless, the BSP sees inflationary risks remaining “toward the upside”, expecting upward pressure to come primarily from potential price increases in transport fares, electricity tariffs, food and oil.

Headline CPI prints mixed in November

Inflation in most of the region’s countries moderated, except in India and Indonesia. Indonesia’s inflation rate climbed to 2.86% YoY in November from 2.56% in October, prompted by an increase in food prices. Stripping out the volatile components of the consumer price index (CPI), core inflation eased to 1.87% from 1.91% in October. Inflation in India also rose; due to higher food prices November headline inflation climbed 5.55% YoY, although the figure came short of the estimated 5.78%. Elsewhere, Singapore’s November inflation numbers eased from the previous month’s spike as prices of transport moderated. The headline CPI rose 3.6% YoY versus the estimated 3.9%, much lower than the October print of 4.7% due to lower contribution from food, housing and utilities. Core inflation was 3.2% YoY, in line with expectations and slightly lower than October’s 3.3%. Price pressures in Malaysia eased further, with the headline inflation rate coming in at 1.5% YoY in November, falling short of the estimated 1.7% and easing from 1.8% YoY in October. The easing was prompted partly by a higher base and slower growth in food prices. Malaysia’s core inflation eased to 2% for the first time since April 2022, moderating for the tenth straight month. In Thailand, consumer prices fell for the second consecutive month; headline inflation declined by 0.44% YoY after dipping 0.31% in October, while core inflation edged up 0.58% after rising 0.66% in October. The headline inflation rate in the Philippines eased to 4.1% YoY in November from 4.9% in October, largely prompted by lower contribution from food components. South Korea’s headline inflation moderated to 3.3% YoY in November, slightly weaker than estimates of 3.5%, after rising 3.8% in October. Core inflation came in at 3.0% in November after rising 3.2% in October.

Market outlook

2024 to be a year of higher returns and lower volatility for Asian local government bonds

2024 is likely to be a year of higher returns and lower volatility for Asian local government bonds with UST yields expected to stabilise and start easing. We expect sentiment toward Asia’s bond markets to turn increasingly positive, attracting capital inflows and providing technical support (through portfolio inflows) that was largely lacking in 2023.

We have an upbeat view of long Indian government bonds due to their attractive carry and favourable technicals. The inclusion of Indian government bonds into JP Morgan’s Government Bond Index-Emerging Markets Index (GBI-EM) from June 2024 is expected to provide support for these bonds.

We believe the broad theme of stronger Asian currencies versus the dollar will dominate in 2024, as we see waning demand for the greenback as the Fed rate hiking cycle comes to an end. The key downside risks to our investment thesis include higher-than-expected energy prices and greater geopolitical uncertainty.

Asian credits

Market review

Asian credits rally in December

Asian credits registered strong gains in December, as credit spreads tightened about 9 bps and UST yields moved sharply lower. Asian IG credit returned 2.69% with spreads narrowing about 7 bps, while Asian HY credit gained 2.01%, with spreads tightening by about 13 bps.

Following the rally by risk assets in November, the markets entered December with continued improvement in overall risk sentiment amid lower global rates as they priced in a more dovish path for the Fed in the coming months. Additionally, positive headlines in China’s property sector contributed to the improvement in sentiment, with immediate liquidity risks being reduced and willingness increasing to conduct asset sales to reduce repayment risk. In mid-December, China’s Central Economic Working Conference focused on a more forceful fiscal policy and a flexible monetary policy. Later in the month Chinese policy makers implemented new measures—with Beijing and Shanghai lowering down payment ratios for first and second homes. Moody’s revising China and Hong Kong’s sovereign rating outlooks to negative from stable was unexpected. However, the revision by Moody’s had minimal impact on most Chinese credits despite the concomitant rating actions on various Chinese banks, state-owned enterprises and select telecommunications, media and technology (TMT) companies. Thin market liquidity heading into the holiday season also magnified the positive risk tone, further supported by the November US CPI which underlined easing inflationary pressures and helped push UST yields lower.

While the dovish Fed was December’s big market theme, slower outflows from emerging market (EM) bond funds also helped boost Asian bonds. These factors, coupled with the near absence of new supply, supported further spread tightening across all major country segments.

USTs rallied in December following the Fed’s dovish pivot at the December FOMC and as expectations of a US economic slowdown increased. While the Fed kept benchmark rates unchanged, the committee acknowledged that growth and inflation were slowing and suggested that the policy rate is at, or close to, its peak level. The dot plot also implied the policy rate being reduced by 75 bps over 2024, 100 bps over 2025 and 75 bps over 2026. UST yields continued their sharp descent after the dovish FOMC meeting, despite attempts by some FOMC members later in the month to push back against the market pricing in deep rate cuts. The benchmark 10-year UST yield settled at 3.88% at the month-end, 44.7 bps lower compared to end-November.

Another month of subdued primary market activity

The primary market was quiet in December, with nearly USD 1.41 billion being raised during the month. The IG space saw just three new issues amounting to USD 800 million, while the HY space had seven new issues amounting to USD 606 million.

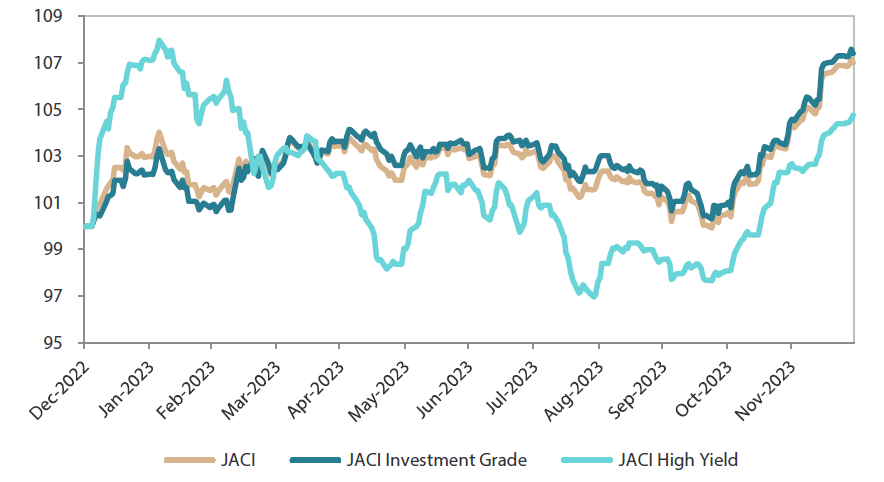

Chart 2: JP Morgan Asia Credit Index (JACI)

Index rebased to 100 at 31 December 2022

Note: Returns in USD. Past performance is not necessarily indicative of future performance.

Source: Bloomberg, 31 December 2023.

Market outlook

Favourable Asia macro backdrop, stable credit fundamentals create historical opportunity to lock in yields

The current macro and market backdrop may see little or minor change, with growth expectations for major economies remaining low and some inflation stickiness resurfacing heading into 2024.

The fundamentals backdrop for Asian credit remains supportive. In China, the recent step-up in fiscal measures suggests that policymakers are aware of the challenging environment. This further raises expectations for policymakers to deliver additional measures to help broaden out China’s recovery and boost economic growth in 2024. Meanwhile, macro and corporate credit fundamentals across Asia ex-China are expected to stay resilient with fiscal buffers despite slower economic growth expectation in the first half of 2024. While non-financial corporates may experience a slight weakening in leverage and interest coverage ratios stemming from lower earnings growth and incrementally higher funding costs, we believe there is adequate ratings buffer for most, especially the IG corporates. Asian banking systems remain robust, with stable deposit base, robust capitalisation and strong pre-provision profitability providing buffers against moderately higher credit costs ahead.

Technically, Asia credit is expected to remain well-supported with lower net new supply as issuers continue to access cheaper onshore funding. Meanwhile, demand remains strong for high quality bonds driven by strong onshore support and pension funds and life insurance companies looking to lock in attractive yields and immunise against long-dated liabilities. Moreover, the consistent outperformance of Asia investment-grade (IG) on a risk-adjusted basis may boost demand and make Asia credit attractive amid the region’s favourable macro backdrop and sufficient fundamental buffer. Key risks include sticky inflation and continued US economic resilience potentially forcing the Fed to continue hiking, as well as rising geopolitical risks. On the other hand, a sudden and sharp weakening of the US labour market and economic activity, coupled with rising delinquencies and defaults, may push spreads wider across global credit. This could exert some pressure on the valuation of Asia IG credit, which continues to look slightly stretched versus historical levels.Technically, Asia credit is expected to remain well supported with lower net new supply as issuers continue to access cheaper onshore funding. Meanwhile, demand remains strong for high quality bonds driven by strong onshore support and pension funds as well as life insurance companies looking to lock in attractive yields. Moreover, the consistent outperformance of Asia IG on a risk-adjusted basis may boost demand and make Asia credit attractive amid the region’s favourable macro backdrop and sufficient fundamental buffer. Nevertheless, following the sharp rally in the past two months, these positive factors have been largely priced in, and the materialisation of some negative risk factors such as a weaker-than-expected global economy may exert some widening pressure on the valuation of Asia IG credit.