You may be like me and get frustrated with the rapidly evolving headlines in the financial press as quotations from political leaders drive bouts of volatility. But there is one headline that persists, and it’s about the relative merits of active investing versus passive alternatives. This headline is often a blanket statement that active investors underperform, which can be demoralising for a practitioner of active investing for nearly 40 years. When you know from experience that the assumption that active investing will underperform is wrong, the polite response is simply “really!”

To be fair there is plenty evidence from various studies that the average active manager doesn’t deliver the goods over most time frames. The difficulty in selecting a manager who will perform should not be confused with the fact that some active managers can consistently achieve higher returns than passive strategies.

This raises the question of what truly differentiates success from failure for an active manager? There is no definitive single answer, but we would suggest the following will help improve your odds of successfully selecting an active alternative to passive.

Essential active ingredients

Selecting both quality managers and companies to invest in portfolios have many common attributes. One of the key challenges is that the plethora of data and information can obscure the most important factors for success. Our Global Equity team’s firm belief is that there are three key ingredients of success that active managers should deliver to make outperformance more likely:

Culture: Investing is tough and complex, it’s best tackled with teams of talent. But great teams need to be cohesive, enjoy working together and most importantly wish to stay together. Strong team culture delivers that.

Philosophical Path: There are many varying paths to delivering long-term active returns, with different volatilities and characteristics, but it is essential that the practitioner knows exactly what path they are on and religiously sticks to it. If your value manager starts sounding like a growth manager, or vice versa, it’s not a good sign.

Process Design: Most managers have an investment process, no doubt with an accompanying flow diagram or funnel. However, the more important question is whether it is well-designed to reinforce team-based decision making and effectively convert philosophy into portfolio returns.

Like when selecting stocks, ensuring that the foundational ingredients are in place is the first key filter. This is the first step in Bayesian probability solving that can make complexity of choice simpler. Analytical diligence on all aspects of a capability’s 4P’s (People, Philosophy, Process and Performance) will help determine whether these ingredients are in place.

Separating the candidates

The essential ingredients are critical but certainly not unique to any one capability, so the next dilemma is how to differentiate the candidates further and increase the probability of selecting an active manager that can actually deliver.

Personally meeting the manager who will be entrusted with your capital, much like meeting the management team as a prospective shareholder, is ideal. However, whether asked directly of via other interactions, the key questions to ask are generally the same. Here are the tough but insightful questions we love to be asked.

- Is your track record as an active manager repeatable as compared to being episodic, dependent on the market fashions of the time or down to luck rather than skill?

- Is decision making dominated by single individuals and if so, how are the inevitable egos, biases and fallibilities managed?

- Are the managers hungry and motivated to keep excelling in their profession?

- Are the investment professionals humble enough to recognise the inevitable mistakes when they happen and in a timely way?

- Are excess investment returns unrelated to the reflexive nature of asset gathering and increased ownership at the security level?

Future Quality investing , the solution we offer, has been delivering since 2011. We are very confident that we have both the ingredients in place and the right answers to all of the above questions. Our objective has been to deliver 3% excess returns (gross), primarily driven by stock selection. Since being backed by Nikko AM as an Edinburgh-based boutique over 10 years ago, we have done exactly that.

So don’t believe the headlines. There are many active managers who can easily justify the role they play in asset owners’ portfolios, and we are proud to be one of them.

You can learn about Future Quality investing via the link below:

https://emea.nikkoam.com/institutional/equity-strategies/global-equity

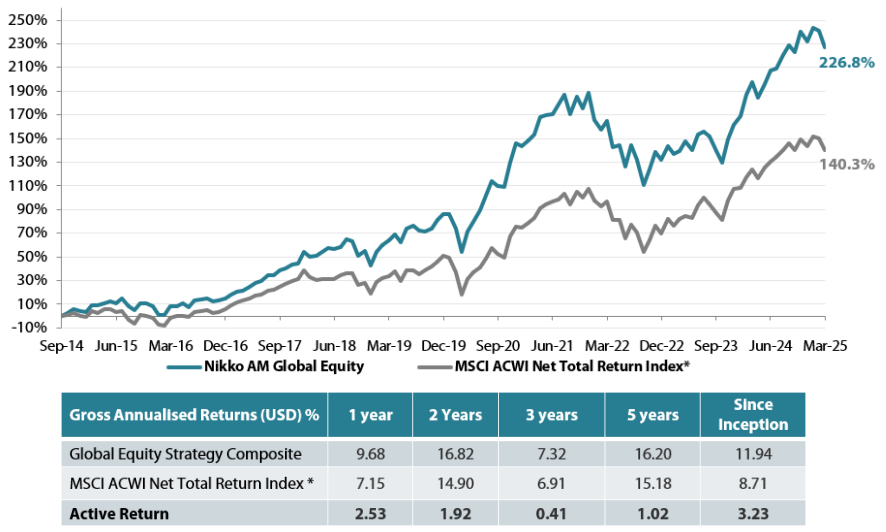

Global Equity strategy composite performance to March 2025

Past performance is not a guide to future returns. Source: Nikko AM, FactSet.

*The benchmark for this composite is MSCI ACWI Net Total Return Index. The benchmark was the MSCI ACWI ex AU since inception of the composite to 31 March 2016. Inception date for the composite is 01 October 2014. Returns are based on Nikko AM’s (hereafter referred to as the “Firm”) Global Equity Strategy Composite returns. Returns for periods in excess of 1 year are annualised. Any comparison to a reference index or benchmark may have material inherent limitations and therefore should not be relied upon.

Data as of 30 March 2025.

Target return is an expected level of return based on certain assumptions and/or simulations taking into account the strategy’s risk components. There can be no assurance that any stated investment objective, including target return, will be achieved and therefore should not be relied upon. Any comparison to a reference index or benchmark may have material inherent limitations and therefore should not be relied upon.

Past performance is not indicative of future performance. Nikko AM Representative Global Equity account. Source: Nikko AM, FactSet.

Nikko AM Global Equity Team

This Edinburgh based team provides solutions for clients seeking global exposure. Their unique approach, a combination of Experience, Future Quality and Execution, means they are continually “joining the dots” across geographies, sectors and companies, to find the opportunities that others simply don’t see.

There are four key areas that make our strategy different:

- a focus on Future Quality companies - a different and clear philosophy

- a distinctive team culture - a tight-knit team with a process built on openness and respect

- unique execution , including rigorous team challenge of every idea

- differentiated portfolios , with a strong track record in stock-picking and ESG integration

Future Quality Companies

We believe that companies with superior long-term returns on investment will deliver better performance. We call these Future Quality companies, and it is only these companies that make it into client portfolios. We search for Future Quality through analysis and financial modelling of companies that we expect to deliver over the next five years, and beyond. This approach is supported by academic evidence that businesses with high and improving returns on invested capital provide superior compound performance over the long term. With this investment time horizon, the sustainability of returns is a crucial ingredient of our Future Quality approach. We have found that companies developing solutions to ESG issues and management teams providing value to all stakeholders are more likely to be successful at sustaining high returns on invested capital over the long-term.

Distinctive team structure and culture

We believe that our collective knowledge and experience are powerful tools for delivering investment performance. Since 2011, we have operated a team-based approach to uncovering Future Quality investment ideas and have fostered a strong group dynamic. Individually, each Portfolio Manager is an expert investor with a broad skillset and experience of many market cycles.

We work in a flat structure, where all our Portfolio Managers have a dual role that combines investment analysis and investment management responsibilities. With individual analytical coverage split along industry lines, each Portfolio Manager is a specialist in the stocks and sectors they cover.

We all actively challenge the ideas and analysis of colleagues throughout the investment process, in an open atmosphere of vigorous and constructive debate. Portfolio Analysts work alongside Portfolio Managers, typically researching thematic trends that could influence and uncover future investment opportunities.

We take collective responsibility for approving stocks for the portfolio, and therefore there is joint accountability for performance. As such, it is in everyone’s interest to ensure that the investment analysis is thorough and that no stone is left unturned in the search for Future Quality.

We believe that the broad experience of our Portfolio Managers and distinctive team-based approach that sees everyone contributing to the strategy, increases the probability of successfully uncovering Future Quality.

Unique execution

Our tight-knit team approach and flat structure enable us to execute in a transparent way, including a rigorous team challenge of every idea. By using our strict Future Quality standards, we can identify long-term winners from the broader universe, to narrow down a comprehensive watch list and around 100 deep dive researched ideas. This is within a unique framework of individual accountability for the underlying analysis and company research, combined with the collective challenging of assumptions at the team level. Our proprietary ranking tool creates a disciplined process to compare and rank attractive opportunities and ensures that at the portfolio construction phase, only our best-ranked ideas receive the most committed weights in client portfolios. We believe our culture is key, and the collective ownership of our research process brings the best portfolio outcomes for clients.

Differentiated portfolios

We deliver a high-conviction Global Equity strategy for clients that is not constrained by benchmarks. As such, Future Quality can be sourced from listed businesses across any geography or sector. And, in a world awash with investment prospects, our disciplined, accountable and transparent process helps us to focus solely on building portfolios from companies that best meet our specific Future Quality criteria.

In terms of balancing risk and reward, our track record shows that we consistently deliver attractive returns on a lower risk-adjusted basis compared with peers and the global reference benchmark. The high active share and concentrated number of holdings help ensure that our Future Quality stock-selection process delivers differentiated portfolios.

Risks

Emerging markets risk - the risk arising from political and institutional factors which make investments in emerging markets less liquid and subject to potential difficulties in dealing, settlement, accounting and custody.

Currency risk - this exists when the strategy invests in assets denominated in a different currency. A devaluation of the asset's currency relative to the currency of the strategy will lead to a reduction in the value of the strategy.

Operational risk - due to issues such as natural disasters, technical problems and fraud.

Liquidity risk - investments that could have a lower level of liquidity due to (extreme) market conditions or issuer-specific factors and or large redemptions of shareholders. Liquidity risk is the risk that a position in the portfolio cannot be sold, liquidated or closed at limited cost in an adequately short time frame as required to meet liabilities of the Strategy.