Summary

- Markets, while volatile, have continued to recover, and we are now seeing an easing of trade tensions. However, in these uncertain times, one thing remains clear—uncertainty itself. The situation remains fluid, and against such a background we expect Chinese policy support to stimulate consumption and business activities.

- Another reason to be constructive on Chinese equities is the country's positive liquidity dynamics, and this could lead domestic institutions to redirect their capital to equity markets for more attractive returns. Elsewhere, India remains a compelling long-term investment opportunity despite short-term challenges; pro-growth consumption policies and structural reforms will likely enable Indian companies to recover in the year ahead.

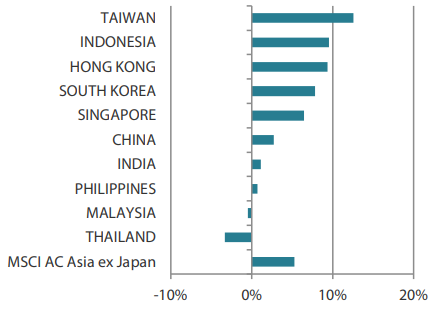

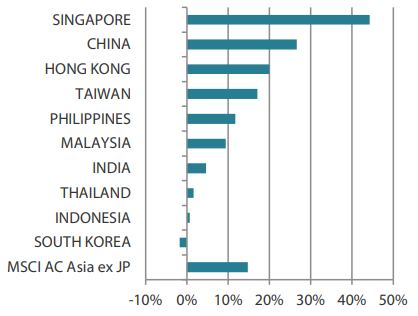

- Markets moved up in May, thanks to the 90-day truce on the US-China tariff war and the US-Britain trade deal, which somewhat eased concerns over global trade. Top-performing Asian markets included Taiwan (+12.5%), Indonesia (+9.6%), Hong Kong (+9.3%) and South Korea (+7.8%), while Thailand (-3.3%) and Malaysia (-0.5%) underperformed.

- While the stock markets of South Korea and Taiwan are among the most sensitive to trade disruption, we have observed several companies already adapting to limit those risks. In ASEAN, amid uncertainties regarding structural reforms and political issues, we prefer the markets of Singapore and Malaysia with their relatively stable politics and tech-driven economic growth.

Market review

Banner month for markets as trade tensions ease

Most of Asia's markets ended May in positive territory, lifted by optimism over progress in trade talks that allayed fears of a tariffs-fuelled global economic slowdown. The UK became the first country to seal an agreement with President Donald Trump since his “Liberation Day” tariff spree. Elsewhere, tensions between the US and China eased, leading to a temporary halt in new duties between the world's two largest economies. Markets welcomed another twist in the Trump trade tariff drama, when a federal trade court deemed his new levies as illegal—although the ruling has since been temporarily put on hold. The MSCI Asia Ex Japan Index advanced 5.3% in US dollar (USD) terms over the month.

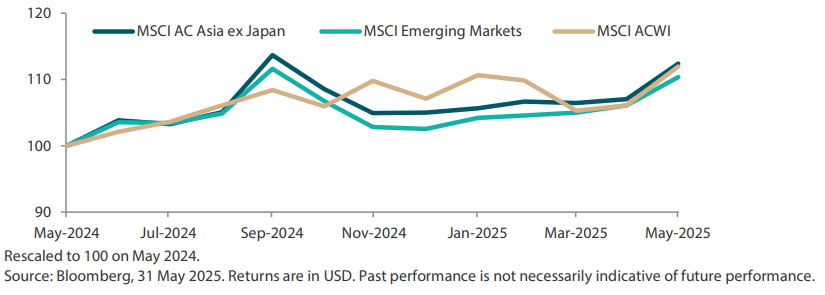

Chart 1: 1-yr market performance of MSCI AC Asia ex Japan vs. Emerging Markets vs. All Country World Index

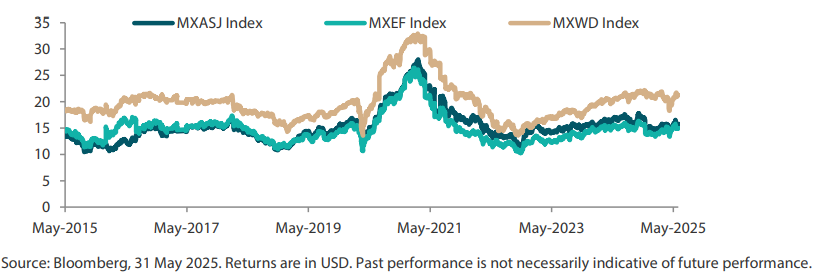

Chart 2: MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index price-to-earnings

Taiwan drives the gains in the region

Tech-heavy Taiwan was one of the region's top performers during the month. Underpinning the market's robust performance, Taiwan's export orders hit a record high of USD 56.4 billion in April, driven by demand for artificial intelligence (AI) applications. Separately, the Taiwan dollar saw an unprecedented surge amid speculation that Washington has pressured them to strengthen the local currency in return for trade concessions. However, Taiwan's central bank has since refuted claims that exchange rates were part of the US trade negotiation. Elsewhere, Indonesia's market was also a top performer within the region. In addition to positive domestic political developments, the market received a boost as Bank Indonesia in May cut key interest rates for the second time this year as it looks to maintain stability of the Indonesian rupiah and to boost economic growth.

Chinese equities were supported as the People's Bank of China cut the benchmark lending rates in a move to boost its economy; the PBOC trimmed the 1-year loan prime rate (LPR) was to 3% from 3.1% and the 5-year LPR to 3.5% from 3.6%. Chinese equities further benefitted from Beijing's agreement with Washington to drastically reduce tit-for-tat tariffs for an initial 90-day period. Hong Kong also welcomed the details of the US-China trade deal.

Chart 3: MSCI AC Asia ex Japan Index 1

For the month ending 31 May 2025

For the year ending 31 May 2025

Source: Bloomberg, 31 May 2025.

1 Note: Equity returns refer to MSCI indices quoted in USD. Returns are based on historical prices. Past performance is not necessarily indicative of future performance.

Market outlook

Chinese policy expected to support to stimulate consumption and business activities

Although they remain volatile, the markets continued to recover following the de-escalation of the Trump administration's “reciprocal” tariffs rhetoric. The most notable development was the US-China agreement announced on 12 May, initiating a 90-days period of tariff reduction effective 14 May, from 145% to 30%. While there notable easing of trade policy tensions, the situation remains uncertain; against such a background we expect Chinese policy support to stimulate consumption and business activities. We continue to see green shoots in China's real estate market, which is showing signs of stabilising, along with a more active stock market rally from a low base.

Another reason to be constructive on Chinese equities is the positive liquidity dynamics in China. Low government bond yields reflect this positive liquidity environment and could prompt domestic institutions to redirect their capital to equity markets for better returns. To that end, China's securities regulator is further encouraging more investments in the equity market by unveiling measures for state-owned insurance firms to invest 30% of annual premiums from new policies in the domestic A-share markets. Despite uncertainty stemming from US tariffs and retaliatory measures from Beijing, there are encouraging signs that the situation may continue to improve.

India remains a compelling destination for long-term investments despite near-term challenges

We believe that India remains a compelling long-term investment opportunity despite short-term challenges it faces. Pro-growth consumption policies and structural reforms may enable Indian companies to recover in the year ahead. We see the Indian market's recent correction as a healthy occurrence that hopefully presents investors with opportunities to invest in some high-quality companies at much more reasonable valuations. We still maintain a cautious view on India, given the challenges in earnings growth faced by its small-cap companies. However, we are aware that there are attractive large-cap companies in India with bottom-up drivers at more attractive valuations.

Several companies in South Korea and Taiwan already adapting to shifting trade patterns

Despite the recent political turmoil characterised by leadership instability and public protests, South Korea has delivered index returns nearing 20% year-to-date on the back of good corporate results and the “Value-up” programme. In South Korea's election held early in June, the opposition's Lee Jae-myung won the presidency after his predecessor Yoon Suk Yeol's impeachment triggered months of chaos. The market's focus should now turn to Lee's policies aimed at shoring up domestic growth, as he has previously pledged and pushed for a supplementary budget. South Korean companies continue to grow globally and deliver good returns at reasonable valuations. The stock markets of South Korea and Taiwan are among the most sensitive to trade disruption, and we observe several companies already adapting to limit those risks.

Singapore and Malaysia the preferred ASEAN markets on relatively stable politics and tech-driven growth

Looking ahead, ASEAN faces uncertainties regarding structural reforms and political issues, which have caused the region to underperform China significantly year-to-date. Thailand is a notable underperformer, experiencing a significant decline in returns with its index sliding more than 12% due to factors such a decline in foreign tourist numbers, concerns over high household debt, political uncertainties and corporate scandals. Meanwhile, Indonesia's index has delivered a 3% return, after experiencing a good recovery in May following positive political developments. Indonesia's stability is highlighted by the absence of major cabinet reshuffles and its state-owned banks being free of military influence for now. Singapore—where the ruling party had just secured a convincing general election victory—and Malaysia remain the preferred countries, benefitting from relatively stable politics and tech-driven economic growth. We continue to believe that structural drivers of fundamental change remain in the region.

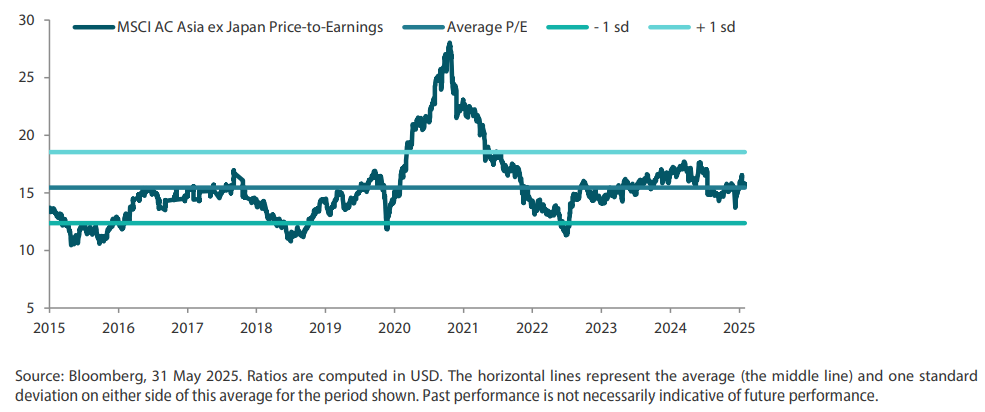

Chart 4: MSCI AC Asia ex Japan price-to-earnings

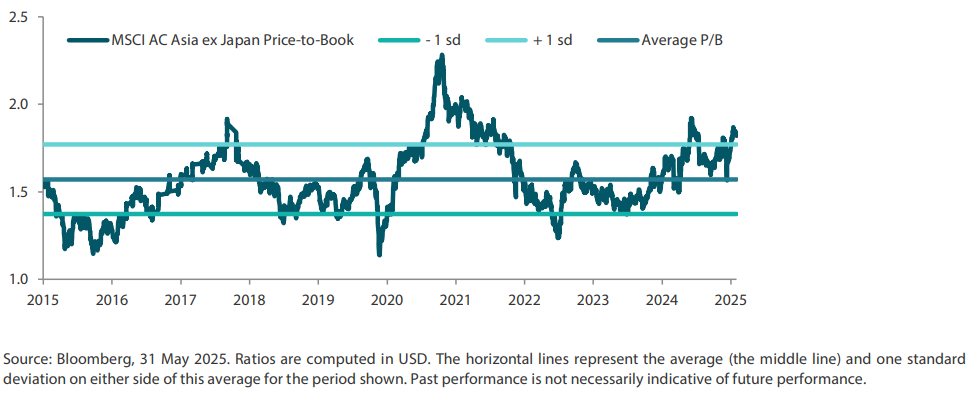

Chart 5: MSCI AC Asia ex Japan price-to-book