Summary

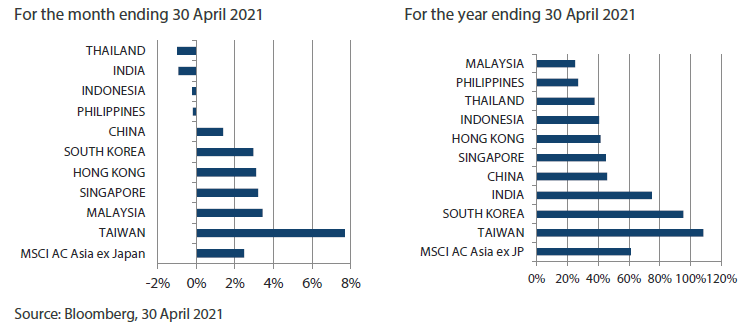

- Asian stocks turned in decent gains in April on optimism about the region’s economic recovery, especially after China and several other Asian countries reported better-than-expected 1Q21 GDP growth. The MSCI AC Asia ex Japan Index gained 2.5% in US dollar (USD) terms over the month.

- Taiwan, Malaysia and Singapore were the best performers in April. Taiwan was buoyed by strength in its electronic and export-oriented stocks, while Malaysia and Singapore posted encouraging economic data.

- Conversely, India lagged on the back of weakness in the Indian rupee amid a severe second wave of COVID-19. China lagged. Thailand and the Philippines also ended the month lower owing to renewed COVID-19 concerns.

- The resurgence of COVID-19 in multiple countries has negative implications for a global recovery. Yet, markets appear to look through these implications, in a show of optimism. Against this backdrop, it appears that the corporate world, and even some large countries, are making tangible moves towards decarbonisation. The ongoing global push towards net zero emissions, should it gain traction, is a tectonic shift with profound global geopolitical and economic implications.

Market review

Regional stocks rebound in April

Rebounding from the previous month’s losses, Asian stocks turned in decent gains in April on optimism about the region’s economic recovery, especially after China and several other Asian countries reported better-than-expected first quarter 2021 (1Q21) GDP growth. Despite renewed COVID-19 fears due to a surge in cases in India and several other Asian countries, regional equities held on to gains for the month, which saw the MSCI AC Asia ex Japan Index rising 2.5% in US dollar (USD) terms. Within the region, Taiwan, Malaysia and Singapore were the best performers (as measured by the MSCI indices in USD terms), while Thailand and India were the worst performers.

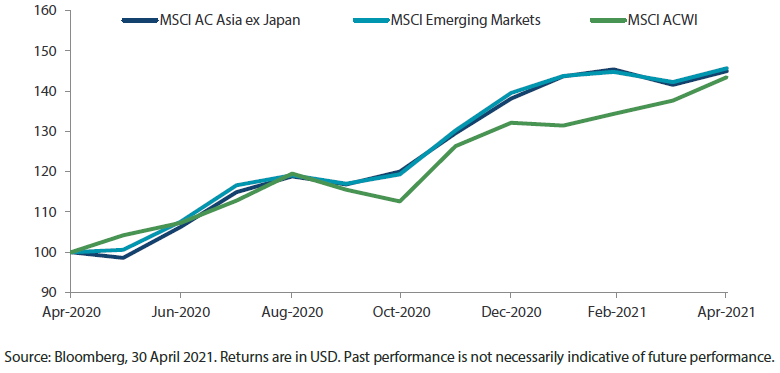

Chart 1: 1-year market performance of MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index

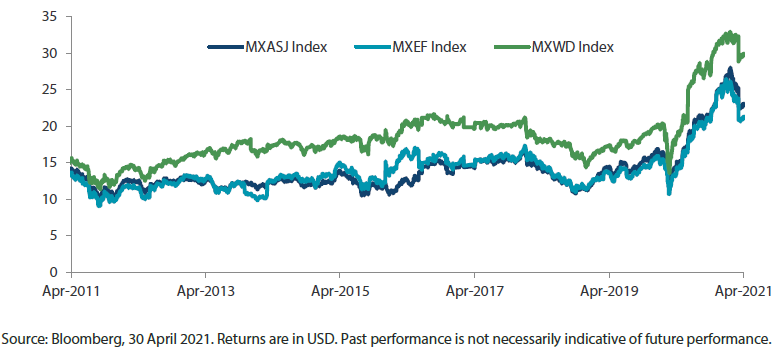

Chart 2: MSCI AC Asia ex Japan versus Emerging Markets versus All Country World Index price-to-earnings

Taiwan outperforms; South Korea, Hong Kong and China track regional rally

In Taiwan, stocks jumped 7.7% in USD terms in April, boosted by the strong performance of electronic and export-oriented stocks amid growing confidence in the global economy. Taiwanese stocks were also lifted by the country’s solid 1Q21 GDP, which grew 8.16% from a year earlier—its fastest pace in more than a decade. In other news, index heavyweight and chip manufacturer Taiwan Semiconductor Manufacturing Company posted a 19.4% rise in 1Q21 net profit due to strong chip demand.

In South Korea, stocks returned 3.0% in USD terms in April. The country's 1Q21 GDP grew at 1.8% year-on-year (YoY), beating market consensus. Index heavyweight and chip giant Samsung Electronics reported a 46% rise in first-quarter net profit, owing to strong profitability at its mobile business.

In other North Asian markets, Hong Kong and China rose 3.1% and 1.4%, respectively, in USD terms in April, supported by the record pace of growth in the world’s second largest economy. Hong Kong financial and consumer staple stocks gained on the back of strong corporate earnings, while Chinese president Xi Jinping’s renewed green pledge bolstered clean energy and electric vehicle (EV) stocks in China.

India underperforms, ASEAN sees mixed returns

In India, stocks fell 0.9% in USD terms for the month, largely on the back of weakness in the Indian rupee amid renewed COVID-19 fears. The country is experiencing an alarming second wave of COVID-19 that has overwhelmed its healthcare system and triggered fresh movement curbs in over 10 states including Delhi and Mumbai.

In the ASEAN region, Malaysia and Singapore turned in respective USD gains of 3.4% and 3.2% in April. Malaysia's exports jumped 31% in March from a year earlier, rising at their fastest pace in nearly four years, while Singapore’s economy grew 0.2% YoY in 1Q21, according to preliminary data, following three consecutive quarters of contraction. Elsewhere, stocks in Thailand and the Philippines fell 1.0% and 0.2% respectively in USD terms for the month, owing to renewed COVID-19 concerns, while Indonesian equities turned in USD losses of 0.2%, weighed down by a downward revision in the country’s 2021 GDP growth by its central bank.

Chart 3: MSCI AC Asia ex Japan Index1

1Note: Equity returns refer to MSCI indices quoted in USD. Returns are based on historical prices. Past performance is not necessarily indicative of future performance.

Market outlook

Markets a function of capital and COVID-19

Successive waves of COVID-19 in multiple countries remind us that the pandemic is not yet a thing of the past. This has negative implications for a global recovery—both in terms of the economic cost (lost economic output, cost of healthcare, inflation squeezing disposable income and geopolitical tensions) and the human cost (death, health impairment and trust deficit). Yet, markets appear to look through these negative implications, in a show of optimism.

So long as capital is cheap, this optimism can be justified. Central banks, notably the US Federal Reserve, are attempting to put off any monetary tightening as long as possible, even as governments are finding ways to ensure continued fiscal stimulus. The ongoing SPAC (special-purpose acquisition company)-mania is another way of ensuring cheap capital; subject to lower regulatory scrutiny, it appears SPACs will exist for longer than expected or warranted.

Global decarbonisation to drive big long-term changes

Against this backdrop, it appears that the corporate world, and even some large countries, are making tangible moves towards decarbonisation. As noted in last month's commentary, the ongoing global push towards net zero emissions, should it gain traction, is a tectonic shift with profound global geopolitical and economic implications. Implementation modalities can have significant and enduring repercussions on supply chains, usage of energy and materials, and relative competitiveness.

China’s green initiatives pave way to greater export competitiveness

China remains committed to a shift in focus from quantity to quality, as well as its "dual circulation" strategy. During the Labour Day holiday, China will initiate a month-long campaign as part of its broader efforts to spur domestic consumption. Policy announcements pertaining to decarbonisation are also sound economically and politically, as it will pave way for greater export competitiveness in a "green" world, based on R&D-driven "climate" technology. The country's focus on greater self-reliance in "traditional" technology, such as 5G and industrial automation, remains unwavering.

South Korea and Taiwan are proxies to digitalisation

Many companies in tech powerhouses South Korea and Taiwan are well positioned to benefit from the increasing digitisation of virtually everything. However, they will need to tread a fine line between China's diplomatic posturing vis-à-vis their traditional ally, the US, given the large end-market offered by the former.

Recovery in India and ASEAN will not be linear

A deadly second wave of COVID-19 infections in India has pushed prospects for a recovery to late 2021 at the earliest. Indian prime minister Narendra Modi's government's poor showing in this regard, however, should not take away from the potentially far-reaching and lasting benefits from the Production Linked Incentive (PLI) scheme in terms of driving India's competitiveness and intellectual property development. This is particularly relevant in emerging areas such as decarbonisation. However, as with all things in India, execution is all-important.

ASEAN is slowly emerging from the pandemic-led economic pain with a potentially enormous opportunity in the "green" economy given the low baseline. A shift away from reliance on oil/coal- fired energy towards renewable sources will improve government finances, and the lower cost of production will offer opportunities in manufacturing. However, messy politics and/or political ennui mean that the path towards realising this potential is bumpy to say the least. In the interim, market consolidation and formalisation of these economies are where the most attractive opportunities lie.

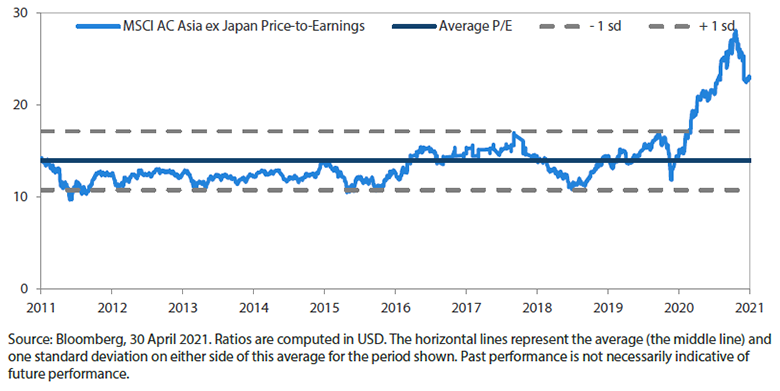

Chart 4: MSCI AC Asia ex Japan price-to-earnings

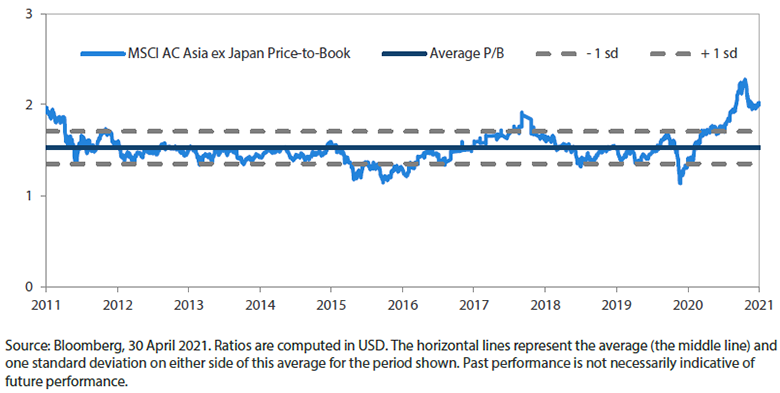

Chart 5: MSCI AC Asia ex Japan price-to-book