In this article, the Asian Equity Team at Nikko AM explores the structural drivers and key factors behind India’s longer-term economic growth trajectory, and the implications for equity investors.

Whether talking about capital deployment, investment or capital flows, India comes to mind as the new preferred destination. Be it capital expenditures by domestic corporates, foreign direct investment (FDI), portfolio flows (both domestic and foreign), and even government spending, India is clearly on a roll.

The India of today is very different to the India we knew ten years ago. The sea-change in investor attitudes and government support for investment is palpable. According to the World Economic Forum (WEF), India is on track to become a US dollar (USD) 10 trillion economy and become the world’s third-largest economy, overtaking Germany and Japan before 2030.1 In fact, WEF President Borge Brende described India as a place with optimism not seen elsewhere in a very “fragmented and polarised world”.2

India accounted for more than 16% of the world’s economic growth in 2023, and in our view, this economic strength is a direct result of government reforms that have been formalising India’s economy and enacting both a digital transformation and an infrastructure boom.

India’s structural reforms to continue

Much of the success can be attributed to the economic leadership under Prime Minister Narendra Modi, who is expected to win the upcoming election for another five-year term later this year. Since 2014, Modi has stuck to the reform path, focusing on transparency, effective spending of public monies and lowering corruption, as well as on improving the ease of doing business in India and cutting red tape.

With an anticipated election victory behind him, and provided Modi achieves the strong voter turnout as expected, we expect this will be viewed as a mandate for the Indian government to continue with its plans for more reforms aimed at promoting economic growth, boosting investment and improving the ease of doing business in areas such as infrastructure development, healthcare, education, agriculture and technology.

India’s digital infrastructure is the envy of the world

Arguably one of the most important reforms put in place during Modi’s premiership has been its flagship “Digital India” programme. Launched in 2015, its central aim is to connect India’s citizens with its government by offering a range of digital products and government services to a diverse population. However, where India differs from anywhere else in the world is that this programme is underpinned by the “India Stack”, a set of open application programming interfaces (APIs) that have revolutionised the way Indian citizens interact digitally. The India Stack is built on the foundation provided by Aadhaar, the world’s largest biometric ID system. Aadhaar has been a cornerstone in the government's efforts towards financial inclusion, bringing more people into the formal banking system, and making it significantly easier for investing in Indian equities, for example.

India's infrastructure boom

Extensive, high-quality infrastructure and an interconnected network of roads, rail and ports, are the foundations for a successful manufacturing economy. Historically, India has been a laggard due to bureaucracy and political hurdles. But in the last decade, things have been improving, and India’s progress in recent years has included overhauling its infrastructure, with the government allocating significant resources towards roads, railways, ports, airports, energy and urban development—see charts below. The scale of these projects, often in partnership with the private sector through public-private partnerships (PPPs), have not only become a key driver of economic growth and job creation, but have also opened up exciting new avenues for overseas investment.

For example, India’s government is planning on developing 35 multi-modal logistics parks (MMLP), with the aim of reducing the logistics costs in India and bringing them to parity with global averages.3 The logistics cost in India is estimated to be around 14% of its GDP compared to 8-10% in Europe and the US. In addition, the successful integration of technology in infrastructure projects, from smart city initiatives to digital platforms for logistics and transportation, has enhanced Indian efficiency and productivity further. Not surprisingly, India has been climbing up the World Bank's Logistics Performance Index rankings, now positioned 38th out of 139 countries, demonstrating that targeted investment in road and port networks and the digitisation of supply chains is bearing fruit.4

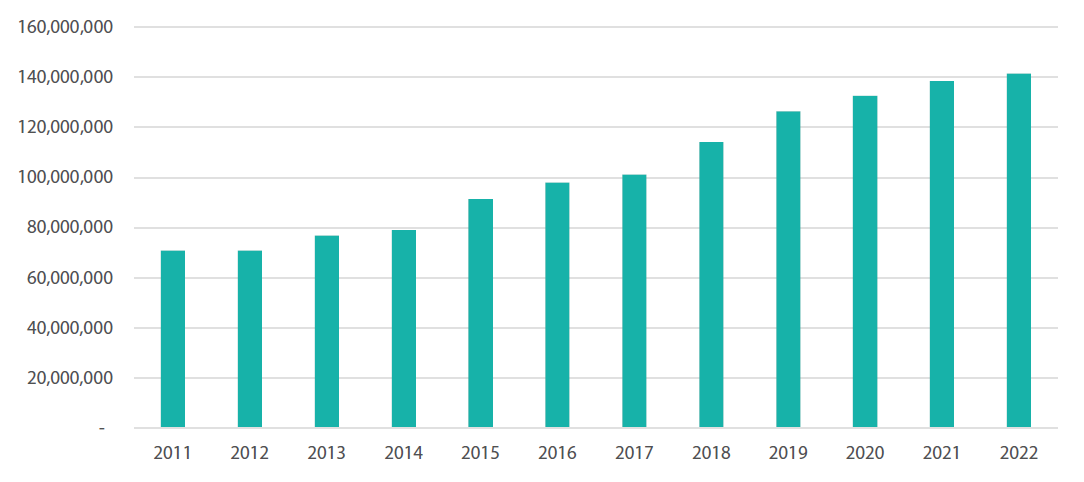

Chart 1: Total length of national highways in India (2011 – 2022) in kilometres

Source: CEIC, Ministry of Road and Transport and Highways (as of 2022)

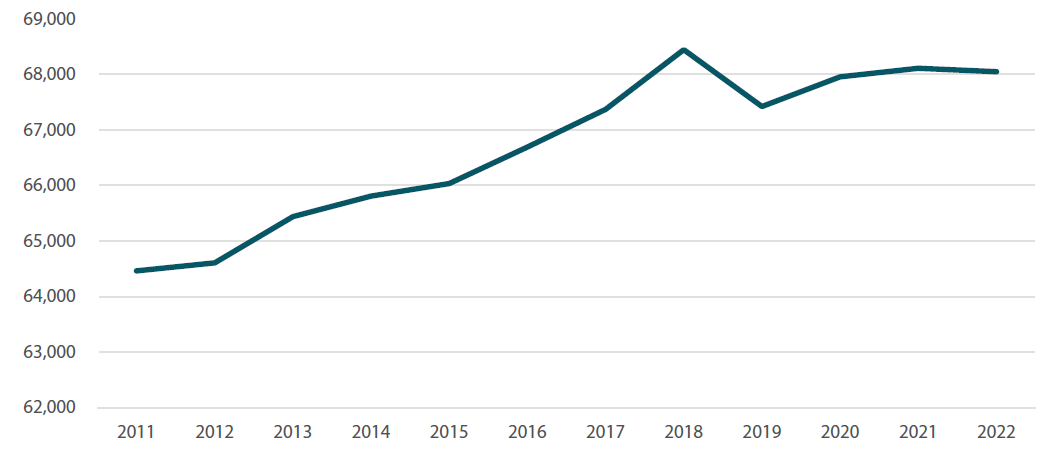

Chart 2: India’s length of railways (route kilometres)

Source: CEIC, India Railways (as of 2022)

Company example 1: Dixon Technologies

A leading player in the electronics outsourcing space, mid-cap stock Dixon has grown its sales and earnings five-fold in the last five years and continues to expand its market footprint. India's electronic manufacturing services (EMS) industry is set to take off on the back of growing demand from both the domestic market and rising outsourcing trends. Significant policy boost via production incentives and other policy measures by the government act as a key tailwind.

The Asia Equity Team identified Dixon as a key beneficiary of the “Make-in-India” and “China +1” trends. Dixon has a large growth runway due to several factors: 1) constant adding to its product portfolio 2) onboarding global brands 3) developing capabilities to increase value-add and 4) massive industry tailwinds. We are impressed with the company’s execution capabilities and the management’s ability to capture growth opportunities with a keen focus on costs. In our view, Dixon can follow in the footsteps of its larger Taiwanese competitors and become a large EMS company in its own right.

Domestic and foreign investment

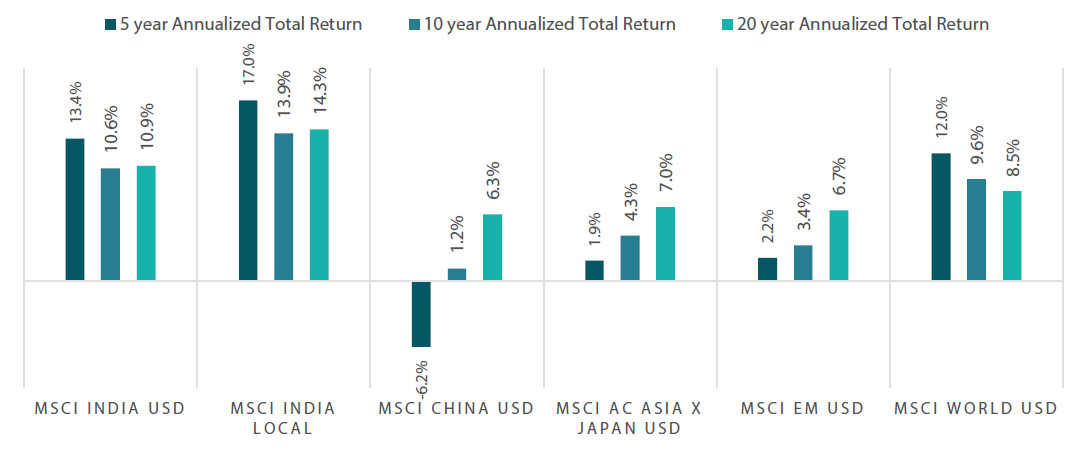

India is now the world’s fifth-largest equity market, behind the US, China, Hong Kong and Japan, although it briefly overtook Hong Kong as recently as January 2024.5 Even so, India’s weighting within the MSCI Global Standard Index is still at 18.2%; with China’s weighting reduced to 25.5%, it leaves ample scope for overseas investors to increase their allocation to Indian companies.6 But for global equity investors, a less-known and sometimes surprising fact is that the portfolio returns in US dollar terms in India have outperformed both their regional peers and developed markets.

Chart 3: India’s equity market is a consistent compounder (annualized total percentage returns)

Source: Bloomberg (as at February 28 2024)

While foreign institutions have been consistently present in the Indian equity market, their exposure by assets under management has doubled in the last decade. India has been a favoured destination for FDI, much more so than its regional ASEAN competitors. In 2022, India attracted more FDI than Vietnam, Malaysia and Indonesia combined. However, what is less talked about is the size and active embrace of equity markets by India’s domestic institutions. These have gone from holding almost no equities in 2014 to holding over USD 120 billion in 2023. As a consequence, the domestic investor is now a very important and active proponent of India’s equity markets.

The result has been notable changes in where foreign direct investments are directed. Industries that were most prominent ten years ago, such as metals, conventional power, tourism and construction are no longer the leaders. Meanwhile, smaller sectors from a decade ago—including computer technology, renewables and pharmaceuticals—have expanded dramatically. Today, 50% of FDI is now invested in “digital’ India”.7 And over the last eight years, about USD 130 billion has been invested in India’s tech start-ups.8 It is therefore not surprising that India now has the third highest number of “unicorns” (start-ups with a valuation of over USD 1 billion) in the world.9

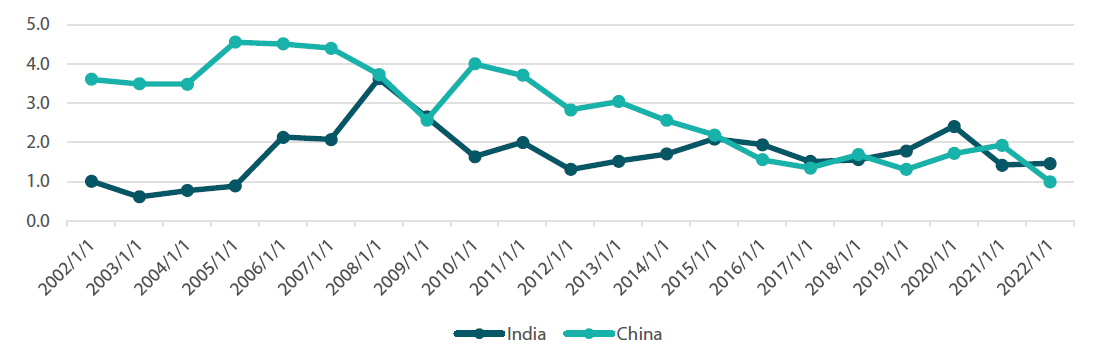

The Asian Equity Team is constantly asked how India compares to China. In the area of FDI, China has been the largest recipient of FDI in the region, which has clearly helped fuel its meteoric growth. However, FDI into China peaked in 2007, has been declining since, and turned negative at the end of last year. It is, therefore, fair to say that China is ex-growth when it comes to FDI flows. By contrast, India has been a steady recipient of FDI flows since the Global Financial Crisis in 2008, and is on the cusp of attracting more flows as it targets becoming a manufacturing and export destination.

Chart 4: foreign direct investment (FDI) as percentage of GDP

Source: World Bank (as of December 31, 2022)

In April 2023, the United Nations reported India had overtaken China as the most populous country in the world. 10Therefore, India needs to achieve a consistent annual growth rate of 7.5% to get close to creating the estimated 70 million new jobs it will need over the next decade. But to get there, the “new” India, one of digitisation, booming infrastructure and manufacturing dominance, will need to replace the “old” India of low-tech manufacturing and an agriculture sector that currently employs 46% of India’s labour force, while only producing 16% of its economic output.11 But if India’s financial services industry can be digitised, there is no reason why its manufacturing and agricultural sectors have to remain stuck in the past.

The investment opportunities present in India

After China, the Indian equity market is the second largest in Asia ex-Japan. A key differentiator of the Indian stock market compared to the Chinese stock market is the prevalence of private companies over state-owned enterprises. Indian private companies are dominated by family or large single owners (or “promoters” to use the local parlance). Though this ownership structure does come with higher corporate governance risks, the broadening out of the share ownership of such companies sets the stage for a higher bar for self-regulation.

Over the last ten years, India’s fastest-growing sector, as a percentage of total market capitalisation, has been financials. In China, for example, it has been information technology and consumer discretionary. Going forward, we believe innovative companies disrupting the staid status quo in sectors such as finance, retailing and manufacturing which have been long dominated by a small number of incumbents, will lead the markets.

Company example 2: Havells India

Havells India, a well-established brand name, manufactures a wide range of consumer durable electrical equipment for both consumer and commercial markets. Through its multi-brand and market segmentation strategy, Havells has aligned itself with the growth of industrial output and the consumer, meaning it is poised for a multi-year growth trajectory. In the next three years, earnings are expected to grow by 20% per year. Havells has the highest total addressable market among its peers and is best placed to benefit from both industry growth and premiumisation. We have a positive view on management’s strategy to focus on the consumer.

Company example 3: PB Fintech

PB Fintech is the “money supermarket” of India. Its offerings include end to-end insurance (Policybazaar) and credit solutions (Paisabazaar) to consumers. These platforms simplify complex choices, present personalised solutions and enable smart financial decisions. Policybazaar has a virtual monopoly in the online channel (>90% share) and continues to grow. Paisabazaar is the latest offering in the consumer credit marketplace. In a country of 1.4 billion with an urban population of 508 million, PB Fintech has only 16 million customers giving it a very long runway for growth. It should become profitable this year and is expected to grow earnings 14-fold in the next three years. India’s financial sectors are evolving to meet the needs of consumers. PB Fintech’s focus on leveraging technology puts it at the forefront of that evolution. We believe PB Fintech is a superior play on the India insurance penetration theme and expansion into new market segments could open up opportunities that are yet to be factored in.

For investors seeking growth potential and stability, backed by robust economic fundamentals underpinned by a forward-thinking reform agenda, India clearly stands out, particularly in comparison to China. However, while global investors might be tempted to replace their China allocation with that of Indian equities, we view that as a false dichotomy.

Both markets offer unique opportunities and challenges that, when combined, can provide a more balanced and diversified strategy for achieving higher risk-adjusted returns. Therefore, with allocations to both China and India, global investors can gain access to two of the world's most dynamic economies, can mitigate risks through geographical and sectoral diversification and can capitalise on the distinct market cycles and economic policies shaping both countries.

If you have any questions on this report, please contact:

Nikko AM team in Europe

Email: This email address is being protected from spambots. You need JavaScript enabled to view it.

7 HSBC, India’s Trajectory, Sept 2023

8 HSBC, India’s Trajectory, Sept 2023

9 Source: Statista

10https://news.un.org/en/story/2023/04/1135967

11 https://www.gbm.hsbc.com/en-gb/insights/global-research/indias-digital-date

Any reference to a particular security is purely for illustrative purpose only and does not constitute a recommendation to buy, sell or hold any security. Nor should it be relied upon as financial advice in any way