Moody's Ratings announced on 16 May a downgrade to the US's formerly top credit rating of Aaa to Aa1. The move by the rating agency was prompted by the US's persistent budget deficits, a risk that we have noted many times before (e.g. in our March quarter GIC Outlook ) and a big reason why we expect the US term premium to remain elevated regardless of the state in which the country's economy finds itself over the mid-term horizon.

It may be said, given the rise in US Treasury bond yields in response to the downgrade, that markets were still surprised by the move, which interrupted an otherwise hope-fuelled rally in US stocks, underpinned by the stability of long-term US bond yields. As we outlined in our Extraordinary GIC Review, April 2025 , however, our most positive scenario (interim volatility followed by trade détente) is just one of many possibilities in a more uncertain world, and financial markets are continuously reassessing the likelihoods of probable outcomes. This shift in thinking within the markets was indeed the catalyst for our adoption of a multi-scenario framework in April, providing a framework to analyse events such as the Moody's downgrade.

Moreover, we draw attention to the US administration's response to bond movements to date, particularly following the announcement of trade tariffs on 2 April and subsequent policy reversals following negative reactions from the bond market. Although the full profile of the payoffs to the US from escalating/de-escalating trade tensions is yet to be revealed, it is likely that US bond yields offer a powerful indicator of an important payoff to the US—the rate at which it finances both its domestic and international liabilities.

The uncertainty surrounding the escalation of trade tariffs, among other policy measures, has made market participants, the US administration, its overseas trade partners and households subject to the constantly shifting contingencies influenced by market reactions to new policy announcements and the response of the US administration to the market. It is particularly helpful to use a Bayesian framework, which enables the updating of existing beliefs priced into the market, to examine the scenarios implicit in market behaviour.

Where are we now? A Bayesian look at bond market moves

We may use our April scenarios to assess the recent bond market moves, harnessing the subjective probabilities that we assigned to each scenario and their respective contingent outcomes by the end of 2025. These scenarios include the following:

- Interim market volatility, followed by trade détente

- Recession with disinflation

- Recession with stagflation

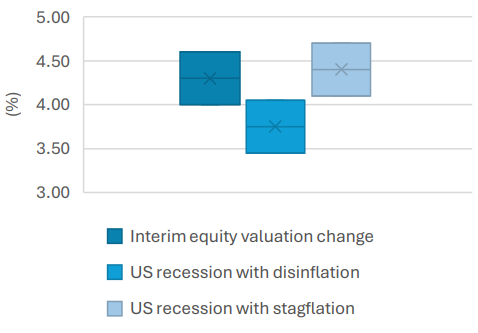

Chart 1 illustrates the expected bond market ranges for each scenario. We recall that our highest-probability scenario as of 10 April was “interim volatility with détente”, which we anticipated would be consistent with bond yields from 4% to modestly above 4.5%. The expected bond yield range for the “recession with stagflation” scenario, however, was skewed higher.

Chart 1: US bond market scenarios (10-year US Treasury yield)

Source: https://en.nikkoam.com/articles/2025/global-investment-committee-review-april-2025

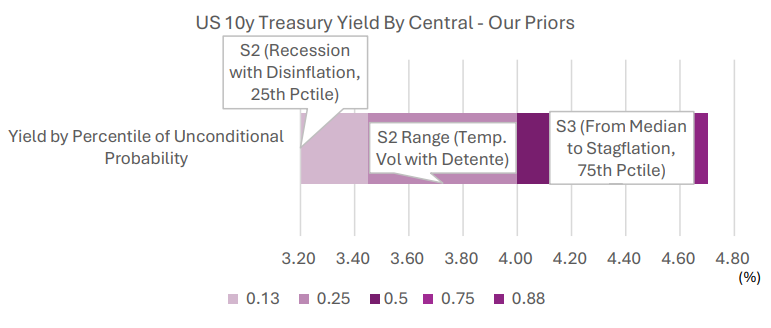

Using a framework of contingent probability to interpret the market's reaction to the Moody's downgrade, yields (at the time of writing ) remain consistent with the upper end of the détente scenario, and the lower end of the “stagflation” scenario.

Updating probabilities to anticipate the US administration's reaction

However, given the high likelihood that bond yields are an important part of the US's payoffs in the ongoing tariff negotiations, it is possible that a further rise in US yields , which may imply a more “stagflationary” expectation from the market (see Chart 2), could influence Washington's policy choices, potentially prompting a shift toward greater “détente” in response to fears of disruptions in the bond market.

Chart 2: Reading US yields - implied scenarios from the US bond market

Source: https://en.nikkoam.com/articles/2025/global-investment-committee-review-april-2025

Why is the bond market so important to the US administration?

Despite the US administration's muscular posturing in trade and its expressed desire to wean itself off of its chronic external deficits, these deficits are closely tied to the advantageous financing rates that the US enjoys on its borrowing at home and overseas. While policymakers may indeed wish to curb external deficits, they are less likely to have the stomach for any sudden spike in US financing rates that would come alongside a sudden adjustment in provision of credit to the world's largest consumer economy.

As such, we could see a temporary spike in US yields followed by a more conciliatory diplomatic tone from the US, even if, as we anticipate, growth is likely to slow even in the most optimistic of US outcomes post the 2 April announcement. Uncertainty is likely to prove a drag on growth in any outcome, but the interaction between the US administration and the bond market is still unfolding.