Higher for longer risks negated by an explosion of generative AI

Before you begin reading, please furnish yourself with a 500 millilitre (ml) bottle of water, imbibe and carry on. Interestingly, this is akin to the water consumption of ChatGPT, which generally “drinks” about 500 ml of water every time you interact with the generative artificial intelligence (AI) chatbot.

Water aside, if one had said the US Federal Funds rates will top 5% and be projected to stay at these levels for years, not months, perhaps one’s decision, thereafter, would be to short or minimise allocation to long-duration assets, high growth stocks and, by virtue, many technology (tech) equity counters.

This highlights why fundamental change is so important. The explosion of generative AI uplifted both sentiment and earnings in large parts of the tech sector and explains why the higher for longer premise for interest rates and inflation has not led to a selloff in tech stocks and tech-centric equity markets in 2023. In fact, the US, Taiwan and South Korea were standout market performers in 2023.

Given that major tech companies are profitable, cash rich and cannot afford to lose out in the highly competitive AI race, spending on high-end computing and neural networks looks set to continue. This will likely create a lasting boon to many component suppliers (the so-called picks and shovels of AI) across Asia.

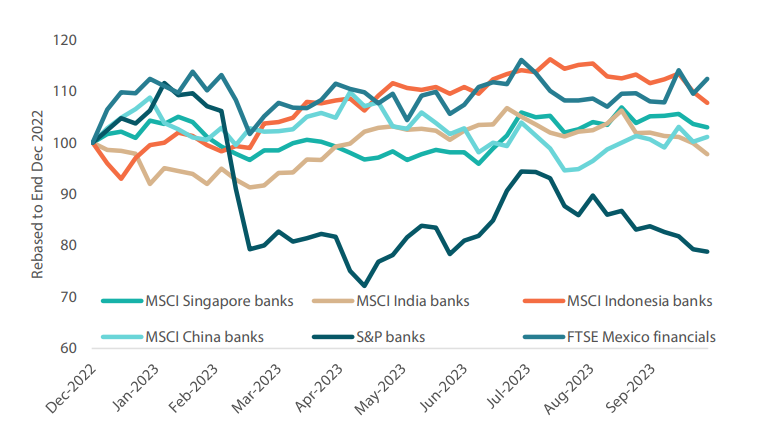

Outperformance of Asian and select emerging market banks

If we look outside of tech, however, other equity market segments paint a different picture. Bank stocks are often good barometers of the health of underlying economies and credit systems. Looking at a sample of Asian and select emerging market banks relative to their US peers, one is led to ask: what fundamental changes are driving such a divergence in performance? (see Chart 1)

Chart 1: Performance of selected country banks year to date

Source: Factset, as at end-October 2023

US bank stocks came under pressure in 2023 for lax regulation, balance sheet vulnerability and sharply higher interest rates. Given the significant maturity transformation and growth in more illiquid private markets since the 2008 Global Financial Crisis, we reckon that the banking sector and many financial institutions, especially those in the developed world, have yet to feel the full effects of higher interest rates.

Likewise, Asian banks have endured sharply higher rates. So why then are bank stocks in the region doing much better? We would point to a combination of structural reforms, supply chain relocation, energy transition-related capital expenditure (capex) and healthy balance sheets. Indian and Indonesian banks were standout performers within the Asian banking sector in 2023.

Leading private banks, such as Bank Central Asia of Indonesia and ICICI Bank of India, currently operate with capital adequacy ratios (CAR) of 29% and 16%, respectively, versus the regulatory required CAR of 12–13%. Credit expansion in both Indonesia and India has been limited relative to their GDPs for years, but this is changing for the better.

Reforms and capex driving India and ASEAN

India has been on a reform drive ever since Prime Minister Narendra Modi was elected in 2014. Since then, the country’s road network has almost doubled and internet penetration has risen from 12% to over 50%. The implementation of the goods and services tax has subsumed 17 indirect taxes, dramatically simplifying the system and improving productivity. Global supply chains are taking note; in 2023 Apple produced 5% of its smartphones, including leading models, in India. Occurring at a time of tightening global liquidity, the recent announcement that Indian government bonds will be included in global bond indices in 2024 is expected to provide a welcome boost to portfolio inflows into India over the coming years. On the whole, India offers an abound of positive fundamental change, and a real capex cycle is also underway.

While parts of ASEAN are seeing renewed investment in their technology sectors, most notably in Malaysia and Vietnam, we believe that it is Indonesia that has the potential for more significant fundamental change. In addition, long overdue reforms, aimed at incentivising more domestic industry developments in areas of healthcare, finance and downstream electric vehicle (EV) manufacturing may provide long-term opportunities.

Focusing on innovation and renewables in China

Turning to the panda in the room, Chinese banks have delivered positive total returns year to date despite a stuttering economy, continued property market deterioration and a crisis of confidence. So, what is going on?

To start with, China’s economy is currently undergoing another major transition—one that prioritises self-sufficiency, advanced manufacturing and directed consumption, as opposed to property- or services-led growth. This has, together with rising geopolitical tensions, understandably led to sustained outflows, particularly from foreign investors. While the broader equity market in China is now trading at all-time low valuations relative to the rest of the Asian region, a selective approach is warranted. There is a marked change in policy that occurred during the summer of 2023 which prioritised the stabilisation of growth. China has always experienced sharp regulatory cycles, with the authorities often using a heavy-handed approach to direct companies towards strategic goals. What has changed is the policy reaction function. No longer will significant credit impulse be used to stimulate activity, which is something the market is still getting used to. It is now about quality, not quantity.

Focusing on underlying innovation and company-specific fundamental change is likely to be a more profitable endeavour for investors over the long term than trying to call the market as a whole. Although it only has limited access to the US auto market, China has overtaken Germany and Japan to be the largest auto exporter globally. Despite significant challenges in accessing leading equipment and high-end chips, Chinese multinational technology company Huawei has successfully launched a smartphone with an in-house designed 7-nanometre chip, which is something that was not thought possible post the US technology restrictions. Similarly, Xiaomi, a leading local smartphone maker in China, recently launched its own mobile operating system.

In the healthcare sector, Chinese companies like biotechnology firm BeiGene and biopharmaceutical company Hutchmed are now competing to be the global best-in-class, while pharmaceutical player Jiangsu Hengrui and Keymed Biosciences (a biotechnology company with multiple clinical-stage assets) could potentially produce first-in-class drugs—something that was unthinkable 10 years ago. Without a doubt, healthcare in Asia has been a huge success story. When we first allocated a dedicated analyst to the sector a decade ago, there were just under 100 investible companies in the region. Now, there are well over 300 companies, with many from China, South Korea and India increasingly becoming global innovators.

Although vast areas of China’s stock market now appear very cheap, it may be worth paying a little more attention to renewables and EV supply chains. We have highlighted before that Net Zero is “made in Asia”; while that may be true, we now have excess supply and some rationalisation of demand, given higher cost of capital and changes in priorities. Major economies still run on oil, and a lack of capex, together with an increasing focus on energy security, is a fundamental change that we expect will last for years in a more geopolitically fractious world. The path of renewables going forward will depend, in our view, on their own capital cycles and supply/demand dynamics, and with valuations of alternative energy now trading below traditional energy companies, it may be time to have closer look (see Chart 2).

Chart 2: MSCI World Alternative Energy (price to book)/MSCI World Energy (price to book)

Source: Bloomberg, as at end-October 2023

New demand on resources spurring fresh opportunities

This brings us back full circle to our opening salvo about water and the overlooked impact today’s changes will have on natural resources.

An average conversation of 5–50 prompts with ChatGPT consumes roughly 500 ml water, according to Shaolei Ren of the University of California and his team in a recent paper (OpenAI channels water from the Raccoon and Des Moines rivers in central Iowa to cool its supercomputers that ChatGPT uses to analyse and decipher human-written texts).

Indeed, water usage is one of the fastest growing areas for both Microsoft and Google. An AI data centre (DC) is estimated to consume 3–20 times the amount of power of a regular enterprise DC, depending on its function and location. Even before the AI DC boom in 2023, enterprise data centre consumption of total energy is seen to have ranged from an average of 1–2% in the European Union to 7% in Singapore (2020) and 18% in Ireland (2022).

These new demands on resources, together with a global energy transition and renewed focus on energy and supply chain security, are causing a significant rethink, which we believe could have large capital expenditure implications. Companies seen benefiting from these trends are likely to be those that provide the following: (1) supply-constrained resources and materials, (2) capital equipment used to reshape grids and (3) efficient solutions to the bottlenecks these new demands create.

2024 may well be another eventful year, and looking more deeply into those underappreciated companies better able to harness the major changes of today is the best way of delivering sustainable returns in the long run, in our view. Out of curiosity, we spent one bottle of water asking ChatGPT its outlook for 2024. One conclusion is that you may still get more water-efficient and insightful results from your equity investment analysts, at least for the time being.

Happy 2024 and good luck for the year ahead.

References to any particular security is purely for illustration purpose only and does not constitute a recommendation to buy, sell or hold any security or to be relied upon as financial advice in any way.