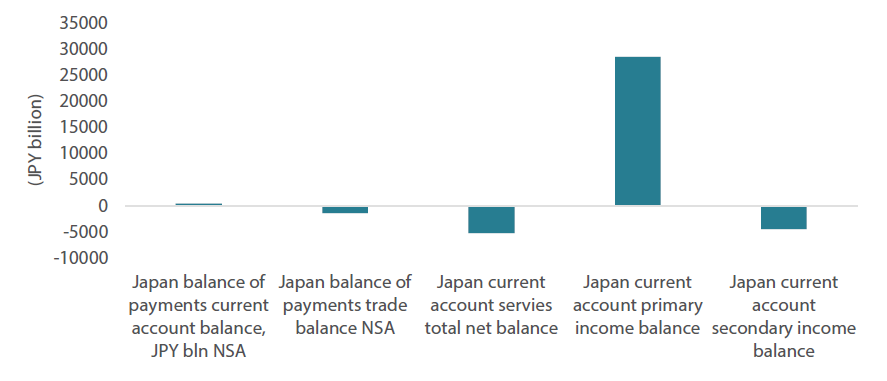

On 19 March, the Bank of Japan (BOJ) joined the other developed economies by returning to traditional tools—short-term interest rates—to govern monetary policy. However, the financial markets seem to understand that Japan’s journey to structural reflation is far from over, and investors appear ready to make the most of ongoing accommodation while it lasts. Policy rates of zero to 10 basis points (bps) and 10-year yields below 80 bps still make for attractive funding conditions for investors to accumulate global assets—both of the “risk-free” sovereign variety and many classes of risk assets thanks to ultra-low volatility. The structure of Japan’s current account shows why it is an opportune time to have a cash surplus in Japan and be able to increase one’s wealth by investing overseas (see Chart 1).

Chart 1: Major Components of Japan’s current account balance

Source: Bloomberg, Nikko Asset Management Global Strategy. Data as at 28 March 2024.

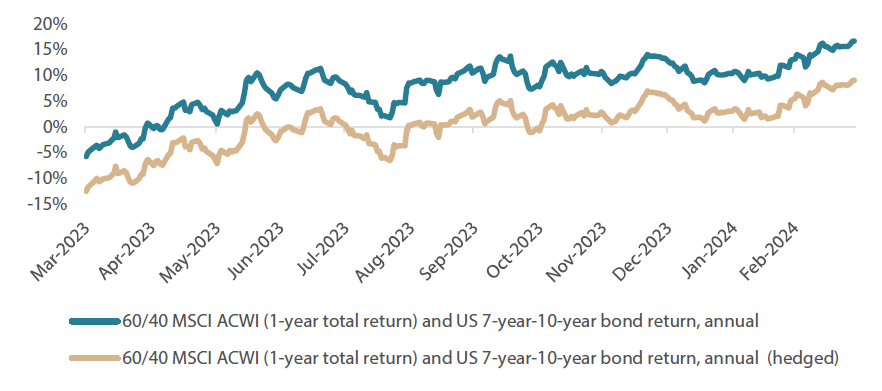

To explore the mechanics of Japan’s enviable income earned on its investments overseas, we examine the returns earned on two multi-asset portfolios, both invested in 60/40 “rule of thumb” allocations to the ACWI (the “risky” asset) and a basket of 7- to 10-year US Treasuries (the “risk-free” asset), both on a yen-hedged (1-year rolling) and yen-funded unhedged basis (Chart 2).

Chart 2: Stock/bond portfolio (60/40), unhedged (funded in yen) and hedged

Source: Bloomberg, Nikko Asset Management Global Strategy. Data as at 28 March 2024.

Even on a fully yen-hedged basis, the returns (above 7%) compare favourably to the annual yield targets of many global institutional investors. Considering the combination of Japan’s relatively muted inflation (and thus, low rates) and a surplus of built-up cash, the Japanese investor should be in the presence of near-ideal global investment conditions. Yet when we look away from institutional investors and turn our focus to the balance sheet of households, we observe that Japanese consumers are taking very little advantage of such conditions. Households have, over the years, built up a formidable stock of cash on their balance sheet, most recently totalling around JPY1.1 quadrillion. However, savings appear stubbornly mired. What is holding consumers back from taking advantage of the gains from relative global yields?

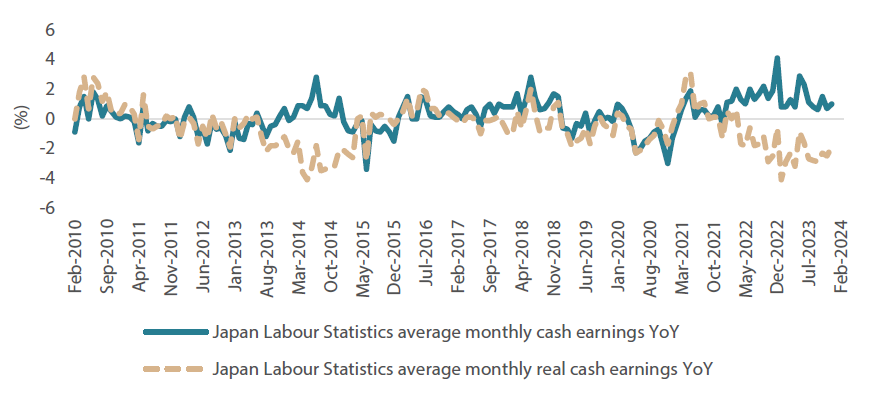

As we have pointed out before, even though Japan’s corporates have been able to benefit from nominal growth to increase their revenues, for Japanese households—as with consumers everywhere—real balances matter. What do we mean by this? Firms have demonstrated their ability to absorb increased import costs, and they have passed them through to consumers. Meanwhile, the only way for consumers to offset price increases is by demanding higher wages. This, all else being equal, increases costs for employers, who then rely on new increases in revenues (i.e., via increased consumption) to maintain profitability. This is the “virtuous circle” that the BOJ has been looking for. But despite nominal wage increases over the last few years, inflation has suppressed real income growth and kept it in negative territory (Chart 3).

Chart 3: Nominal versus real labour cash earnings

Source: Bloomberg, Nikko AM Global Strategy. Data as at 21 February 2024.

With the historic wage increases garnered by Japan’s labour unions in its “shunto” spring negotiations, there are credible reasons to expect real income growth to turn positive in 2024. Nonetheless, sustained positive real income growth has yet to be realised in the data, and this is one important development that the BOJ is likely waiting for before it withdraws any further accommodation. Alongside such real income growth, the BOJ is likely to be looking for consumer surpluses to be allocated not to building up cash deposits, such as was the case during Japan’s “lost decades”, but to increasing their consumption. This would assist GDP growth and also put money to work in financial markets.

Households’ shift to reflationary behaviour: much awaited, not yet realised

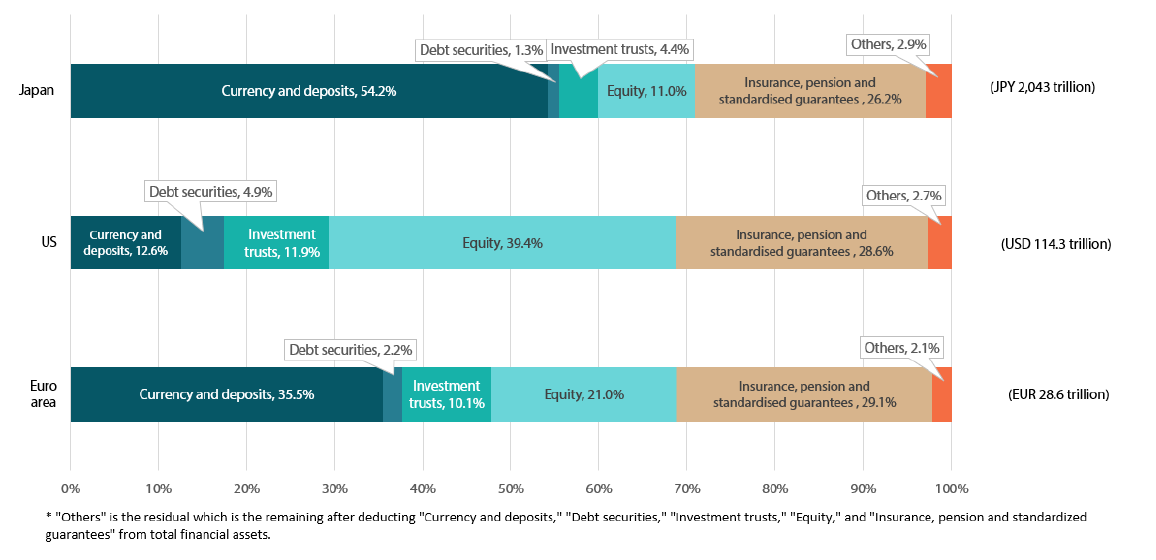

There are compelling reasons to believe that households will oblige and increase their consumption. Even if consumption growth increases by a modest gradient, it would occupy a large share of Japan’s GDP, making it more powerful than an equivalent expansion in net exports. The other part of household behaviour that may show a reflationary pivot is household investment. Although building up cash savings—even in a zero interest rate environment—is fully rational in a deflationary economy, doing so amid even mild reflationary conditions is not. Households were long under-invested in financial markets by global comparison (see Chart 4). However, reflation provides a monetary incentive for households to participate in financial markets and to seek returns at least capable of keeping up with inflation.

Chart 4: Comparison of household balance sheets

Source: BOJ. Data as at August 2023.

On this front, the new Nippon Individual Savings Account (NISA) regulations that took effect in 2024 are well timed. Not only do NISA's tax benefit incentives encourage the accumulation of long-term savings in financial market instruments, but they also provide incentives for market entry in the current year. In addition, they open the door to the exponential benefits of compounding over time, a phenomenon that Western market players often refer to as “the eighth wonder of the world”. The enhanced NISA program’s focus on cumulative savings benefits household balance sheets. It encourages “dollar cost averaging” behaviour, as opposed to the “theme rotation” strategy popular among active household investors. This discourages “market timing”, a strategy that both institutional investors and households often struggle to execute consistently, leading to poor results.

Another piece of the puzzle: financial literacy

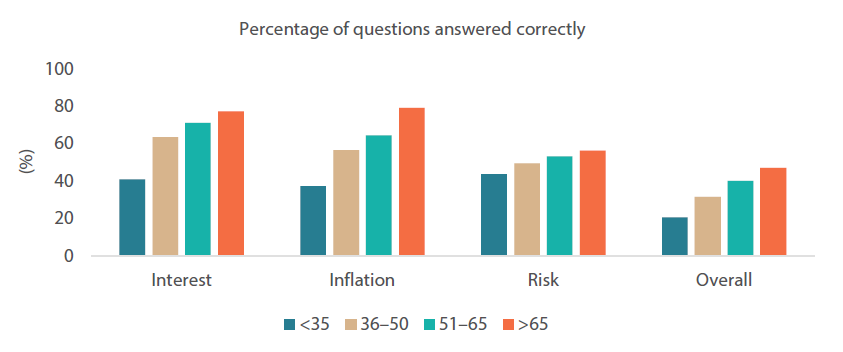

Japanese households’ lack of interest in financial markets may soon change once they realise they have been missing out as Japanese indices break consecutive historical records. Nonetheless, old habits die hard, and the deflationary mindset prevalent among households may require particular effort to overcome. One area where deflation has eroded household interest and capability to participate in financial markets has been household financial literacy.

Chart 5: Japanese financial literacy by age

Source: Sticha, Andrea, & Shizuka Sekita (2023). The importance of financial literacy: Evidence from Japan. Journal of Financial Literacy and Wellbeing 1, 244–262. https://doi.org/10.1017/flw.2023.9

Chart 5 illustrates simple measures of financial literacy, focusing on three key topics: interest, inflation and risk. It shows that a clear divide in financial literacy exists between older and younger households, with deflation and zero to negative interest rates likely to have curtailed the understanding of key financial concepts among the younger generations.

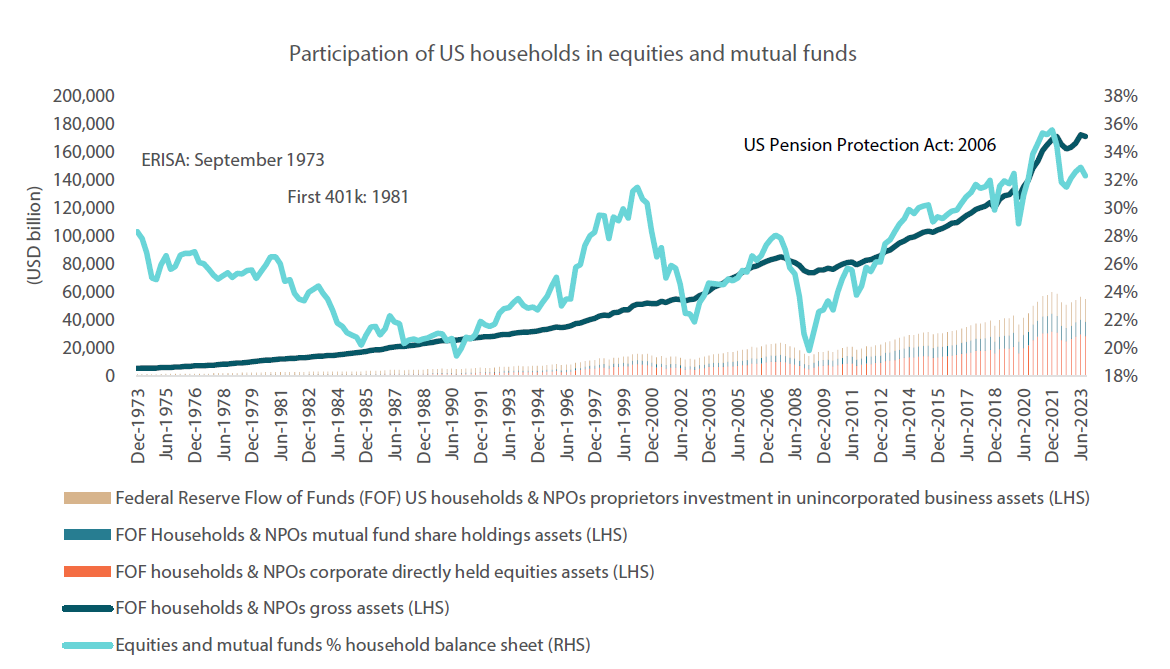

Insufficient financial literacy may be one reason why significant participation by households is yet to be observed. Greater participation, once it occurs, may bring significant benefits to households; it could also aid the overall development of financial markets. In the US, gradual policy shifts favouring greater participation by households in financial markets—such as ERISA, the growth of defined contribution programs, the Pension Protection Act of 2006, the Secure Act and Secure Act 2.0—have greatly increased the demand for financial market assets (Chart 6).

Chart 6: US retirement savings legislation history and household financial participation

Source: Bloomberg, US Federal Reserve, Nikko AM Global Strategy. Data as at 24 February 2024.

Considering that Japan remains a developed economy with a mature household likely to spend time and money on education, we can assume that the generational gaps in financial literacy may be bridged over time. Nonetheless, this is likely an area both the government and BOJ will be keenly monitoring for signs that the “virtuous circle” remains in motion.